Cologne Corporation is considering a new project requiring a $25,000 investment in an asset having no sal-

vage value. The project would produce $15,000 of pretax income before depreciation at the end of each of the

next six years. The company's income tax rate is 30%. In compiling its tax return and computing its income

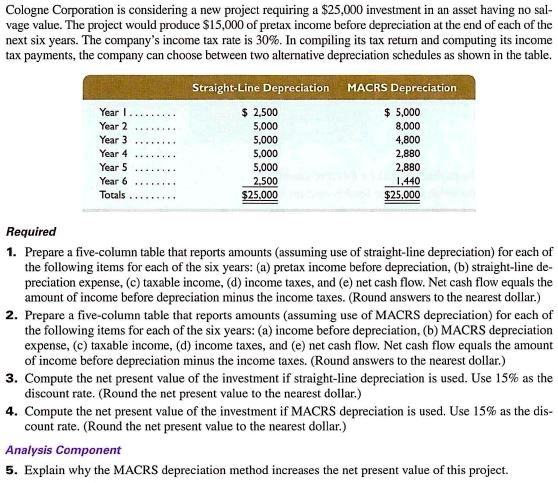

tax payments, the company can choose between two alternative depreciation schedules as shown in the table.

Straight-Line Depreciation

MACRS Depreciation

Year I

$ 2,500

$ 5,000

Year 2

5,000

8,000

Year 3

5,000

4,800

Year 4

5,000

2,880

Year 5

5,000

2,880

Year 6

2,500

1,440

Totals

$25,000

$25,000

Required

1. Prepare a five-column table that reports amounts (assuming use of straight-line depreciation) for each of

the following items for each of the six years: (a) pretax income before depreciation, (b) straight-line de-

preciation expense, (c) taxable income, (d) income taxes, and (e) net cash flow. Net cash flow equals the

amount of income before depreciation minus the income taxes. (Round answers to the nearest dollar.)

2. Prepare a five-column table that reports amounts (assuming use of MACRS depreciation) for each of

the following items for each of the six years: (a) income before depreciation, (b) MACRS depreciation

expense, (c) taxable income, (d) income taxes, and (e) net cash flow. Net cash flow equals the amount

of income before depreciation minus the income taxes. (Round answers to the nearest dollar.)

3. Compute the net present value of the investment if straight-line depreciation is used. Use 15% as the

discount rate. (Round the net present value to the nearest dollar.)

4. Compute the net present value of the investment if MACRS depreciation is used. Use 15% as the dis-

count rate. (Round the net present value to the nearest dollar.)

Analysis Component

5. Explain why the MACRS depreciation method increases the net present value of this project.