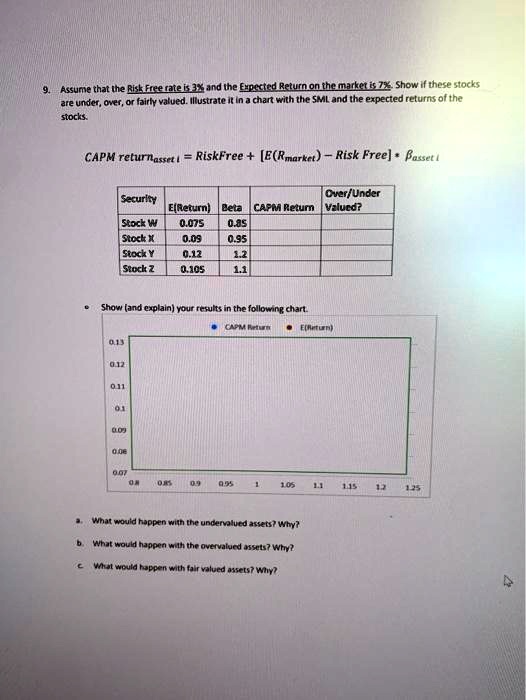

9. Assume that the Risk Free rate is 3% and the Expected Return on the market is 7%. Show if these stocks

are under, over, or fairly valued. Illustrate it in a chart with the SML and the expected returns of the

stocks.

CAPM returnasset = RiskFree + [E(Rmarket)- Risk Free] \cdot \beta_{asset} i

Security

Over/Under

E(Return) Beta CAPM Return Valued?

Stock W 0.075 0.85

Stock X 0.09 0.95

Stock Y 0.12 1.2

Stock Z 0.105 1.1

Show (and explain) your results in the following chart.

0.13

0.12

0.11

CAPM Return

E(Return)

0.09

0.08

0.07

0.8

0.85

0.9

0.95

1

1.05

1.1

1.15

1.2

1.25

a. What would happen with the undervalued assets? Why?

b. What would happen with the overvalued assets? Why?

c. What would happen with fair valued assets? Why?