ACTIVITY. 1

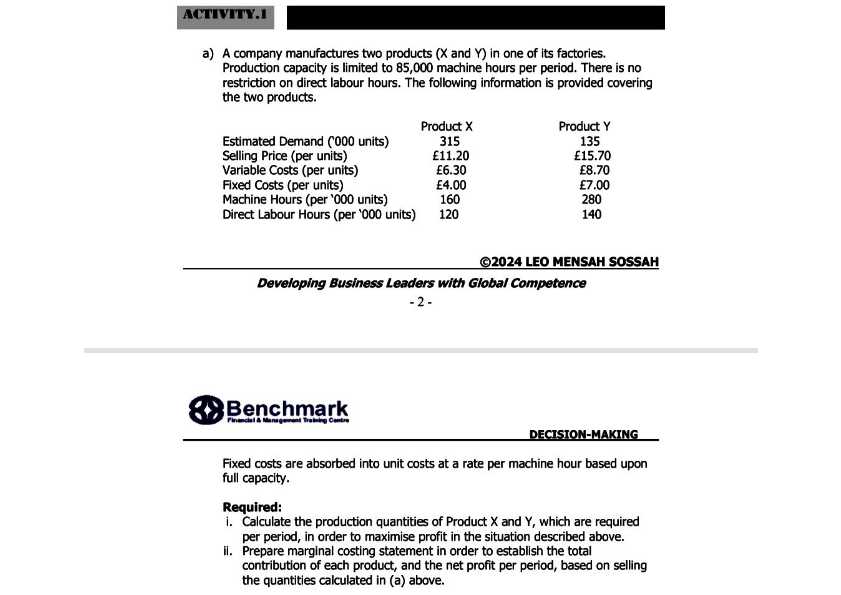

a) A company manufactures two products ( \( X \) and \( Y \) ) in one of its factories. Production capacity is limited to 85,000 machine hours per period. There is no restriction on direct labour hours. The following information is provided covering the two products.

\begin{tabular}{lcc}

& Product \( X \) & Product Y \\

& 315 & 135 \\

Estimated Demand (co00 units) & \( £ 11.20 \) & \( £ 15.70 \) \\

Selling Price (per units) & \( £ 6.30 \) & \( £ 8.70 \) \\

Variable Costs (per units) & \( £ 4.00 \) & \( £ 7.00 \) \\

Fixed Costs (per units) & 160 & 280 \\

Machine Hours (per '000 units) & 120 & 140 \\

Direct Labour Hours (per '000 units) & 120 &

\end{tabular}

(c)2024 LEO MENSAH SOSSAH

Developing Business Leaders with Global Competence -2 -

Benchmark

DECISION-MAKING

Fixed costs are absorbed into unit costs at a rate per machine hour based upon full capacity.

Required:

1. Calculate the production quantities of Product \( X \) and \( Y \), which are required per period, in order to maximise profit in the situation described above.

ii. Prepare marginal costing statement in order to establish the total contribution of each product, and the net profit per period, based on selling the quantities calculated in (a) above.