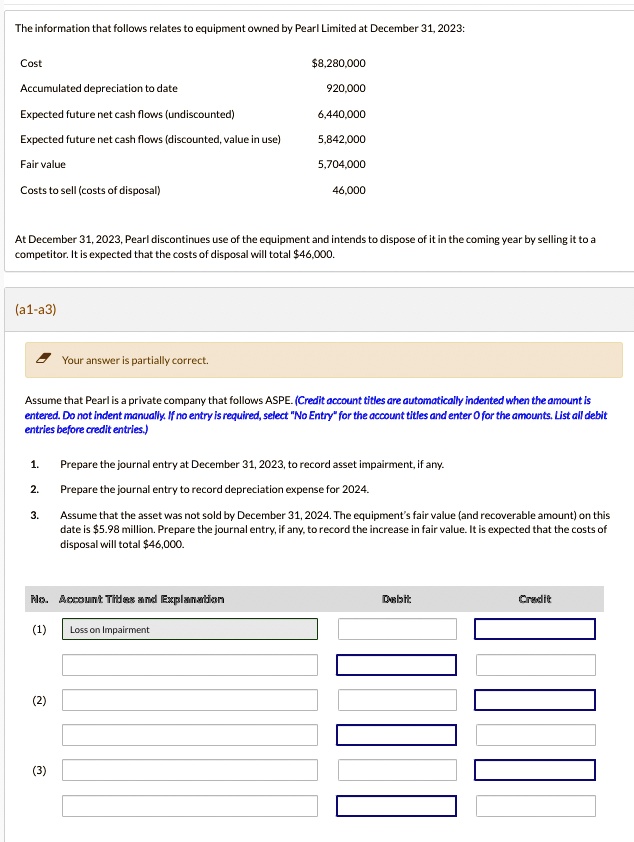

The information that follows relates to equipment owned by Pearl Limited at December 31, 2023:

Cost

$8,280,000

Accumulated depreciation to date

920,000

Expected future net cash flows (undiscounted)

6,440,000

Expected future net cash flows (discounted, value in use)

5,842,000

Fair value

5,704,000

Costs to sell (costs of disposal)

46,000

At December 31, 2023, Pearl discontinues use of the equipment and intends to dispose of it in the coming year by selling it to a

competitor. It is expected that the costs of disposal will total $46,000.

(a1-a3)

Your answer is partially correct.

Assume that Pearl is a private company that follows ASPE. (Credit account titles are automatically indented when the amount is

entered. Do not indent manually. If no entry is required, select \"No Entry\" for the account titles and enter 0 for the amounts. List all debit

entries before credit entries.)

1.

Prepare the journal entry at December 31, 2023, to record asset impairment, if any.

2.

Prepare the journal entry to record depreciation expense for 2024.

3.

Assume that the asset was not sold by December 31, 2024. The equipment's fair value (and recoverable amount) on this

date is $5.98 million. Prepare the journal entry, if any, to record the increase in fair value. It is expected that the costs of

disposal will total $46,000.

No. Account Titles and Explanation

(1)

Loss on Impairment

(2)

(3)

Debit

Credit