FITNESS-FOR-ALL

F Y2026 ANALYSIS

Appendix IV - Defined Benefit Plan

On July 1, 2026, FFA implemented a defined benefit plan to entice its employees to stay for years

to come. To really encourage employees to stay, FFA ensured that the plan would be non-

contributory for all employees. In other words, only FFA would need to contribute, while the

employees would benefit from the amounts when they retire.

Stephanie deemed $230,000 to be suitable for past service costs. No contributions have been

made from FFA for current service costs, and $120,000 has been contributed from FFA for past

service costs.

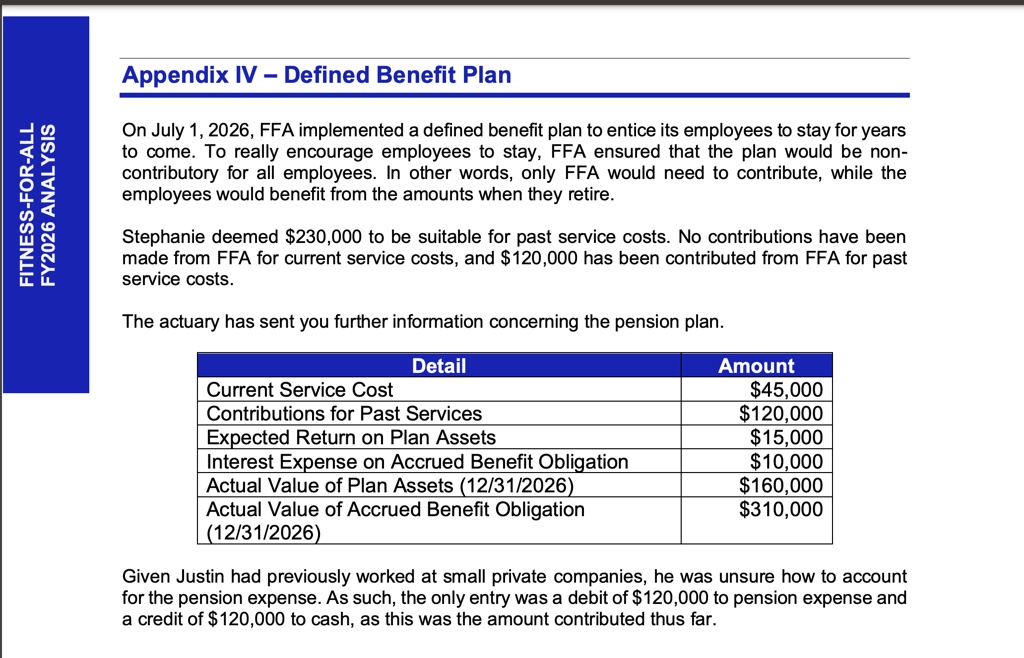

The actuary has sent you further information concerning the pension plan.

Detail Amount

Current Service Cost $45,000

Contributions for Past Services $120,000

Expected Return on Plan Assets $15,000

Interest Expense on Accrued Benefit Obligation $10,000

Actual Value of Plan Assets (12/31/2026) $160,000

Actual Value of Accrued Benefit Obligation $310,000

(12/31/2026)

Given Justin had previously worked at small private companies, he was unsure how to account

for the pension expense. As such, the only entry was a debit of $120,000 to pension expense and

a credit of $120,000 to cash, as this was the amount contributed thus far.