This is an advanced microeconomics class, and the question is about certainty equivalence and the Arrow-Pratt coefficient.

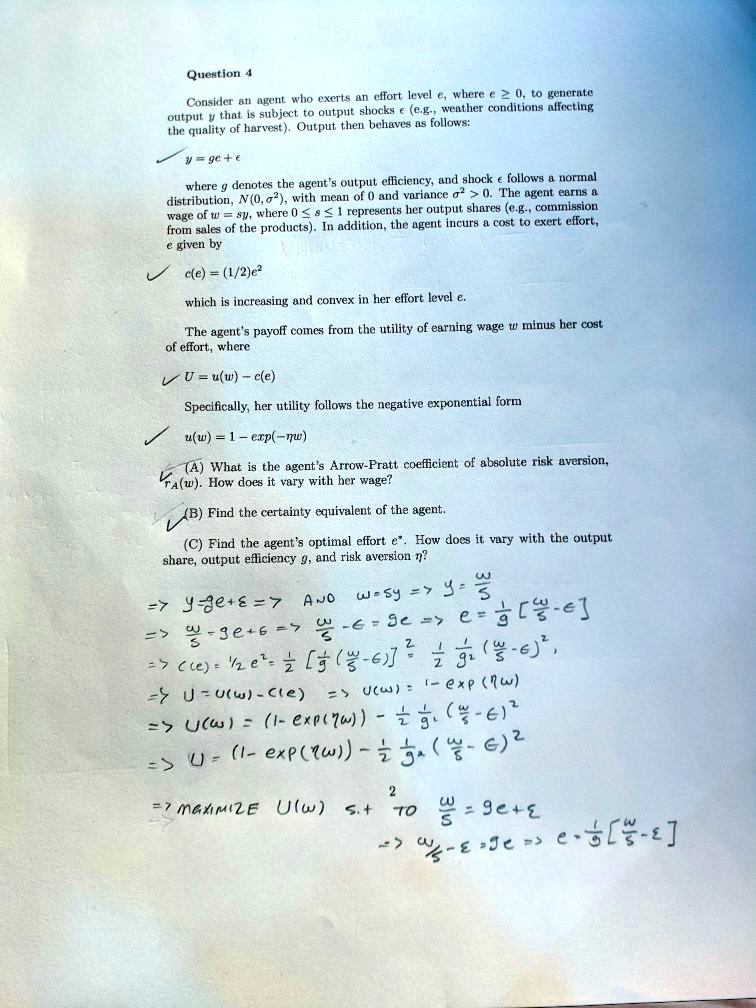

Question 4:

Output y is subject to output shocks e (e.g. weather conditions affecting the quality of the harvest). Output then behaves as follows:

y = ge + e, where g denotes the agent's output efficiency, and shock e follows a normal distribution N(0,2) with a mean of 0 and variance o > 0. The agent earns a wage of w = sy, where 0 < s < 1 represents her output shares (e.g. commission from sales of the products). In addition, the agent incurs a cost to exert effort, e, given by ce = 1/2e, which is increasing and convex in her effort level e. The agent's payoff comes from the utility of earning wage w minus her cost of effort, where

U = uw - ce. Specifically, her utility follows the negative exponential form w = 1 - exp(-mw).

A) What is the agent's Arrow-Pratt coefficient of absolute risk aversion, raw? How does it vary with her wage?

B) Find the certainty equivalent of the agent.

C) Find the agent's optimal effort, e. How does it vary with the output share, output efficiency g, and risk aversion n?

=7maxim2EU(ws.+TO [3-3]2=23-m-