Chapter 8: Budgeting for Planning and Control

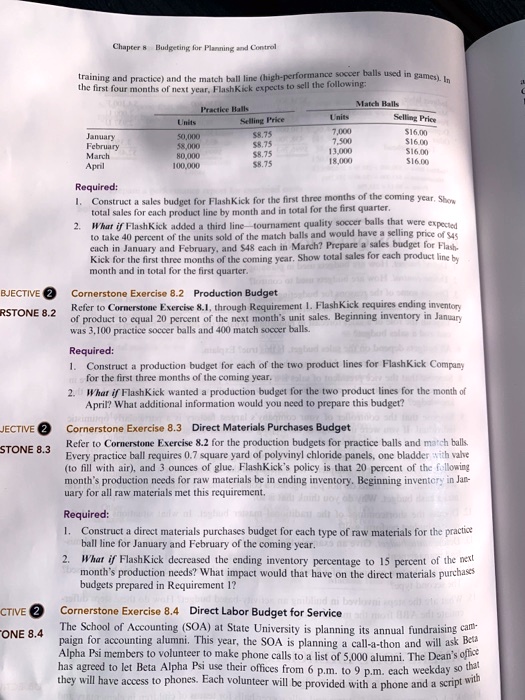

Practice Balls Units Selling Price 50,000 $8.75 58,000 $8.75 80,000 $8.75 100,000 $8.75

Match Balls Units Selling Price 7,000 $16.00 7,500 $16.00 13,000 $16.00 18,000 $16.00

January February March April

Required:

Total sales for each product line by month and in total for the first quarter.

Objective 2: Cornerstone Exercise 8.2 - Production Budget

Refer to Cornerstone Exercise 8.1, through Requirement 1. Flash Kick requires ending inventory of product to equal 20 percent of the next month's unit sales. Beginning inventory in January was 3,100 practice soccer balls and 400 match soccer balls.

Required:

Construct a production budget for each of the two product lines for Flash Kick Company for the first three months of the coming year.

What if Flash Kick wanted a production budget for the two product lines for the month of April? What additional information would you need to prepare this budget?

Objective: Cornerstone Exercise 8.3 - Direct Materials Purchases Budget

Refer to Cornerstone Exercise 8.2 for the production budgets for practice balls and match balls. Every practice ball requires 0.7 square yard of polyvinyl chloride panels, one bladder with valve to fill with air, and 3 ounces of glue. Flash Kick's policy is that 20 percent of the following month's production needs for raw materials be in ending inventory. Beginning inventory in January for all raw materials met this requirement.

Required:

Construct a direct materials purchases budget for each type of raw materials for the practice ball line for January and February of the coming year.

What if Flash Kick decreased the ending inventory percentage to 15 percent of the next budget prepared in Requirement 1?

Objective 2: Cornerstone Exercise 8.4 - Direct Labor Budget for Service