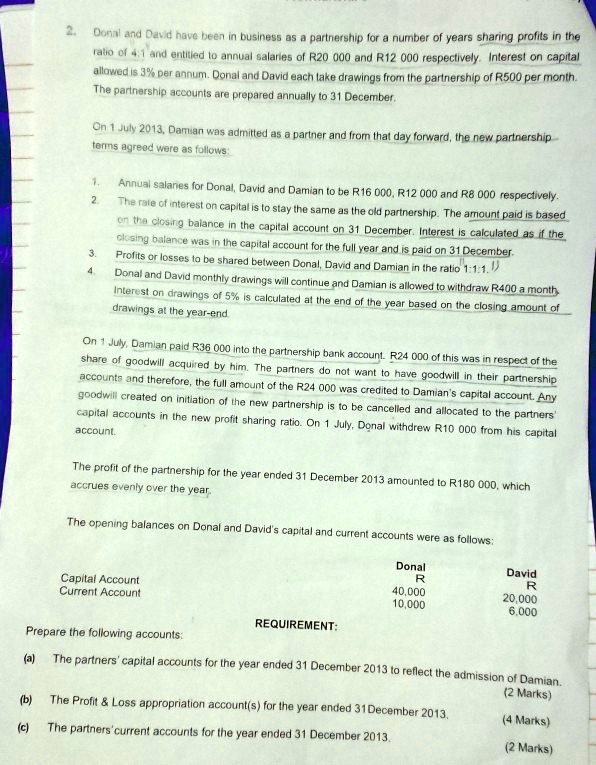

The ratio of 41 and entitled to annual salaries of R20,000 and R12,000 respectively. Interest on capital. The partnership accounts are prepared annually to 31 December. The terms agreed were as follows:

1. The rate of interest on capital is to stay the same as the old partnership. The amount paid is based on the closing balance in the capital account on 31 December. Interest is calculated as if the closing balance was in the capital account for the full year and is paid on 31 December.

2. Interest on drawings of 5% is calculated at the end of the year based on the closing amount of drawings at the year-end.

3. Share of goodwill acquired by him. The partners do not want to have goodwill in their partnership accounts and therefore, the full amount of the R24,000 was credited to Damian's capital account. Any goodwill created on initiation of the new partnership is to be cancelled and allocated to the partners' capital accounts in the new profit sharing ratio.

On 1 July, Donal withdrew R10,000 from his capital.

The profit of the partnership for the year ended 31 December 2013 amounted to R180,000, which accrues evenly over the year.

The opening balances on Donal and David's capital and current accounts were as follows:

Donal Capital Account: R40,000

Donal Current Account: R10,000

David Capital Account: R20,000

David Current Account: R6,000

REQUIREMENT: Prepare the following accounts:

(a) The Profit & Loss appropriation account(s) for the year ended 31 December 2013.

(b) The partners' current accounts for the year ended 31 December 2013.