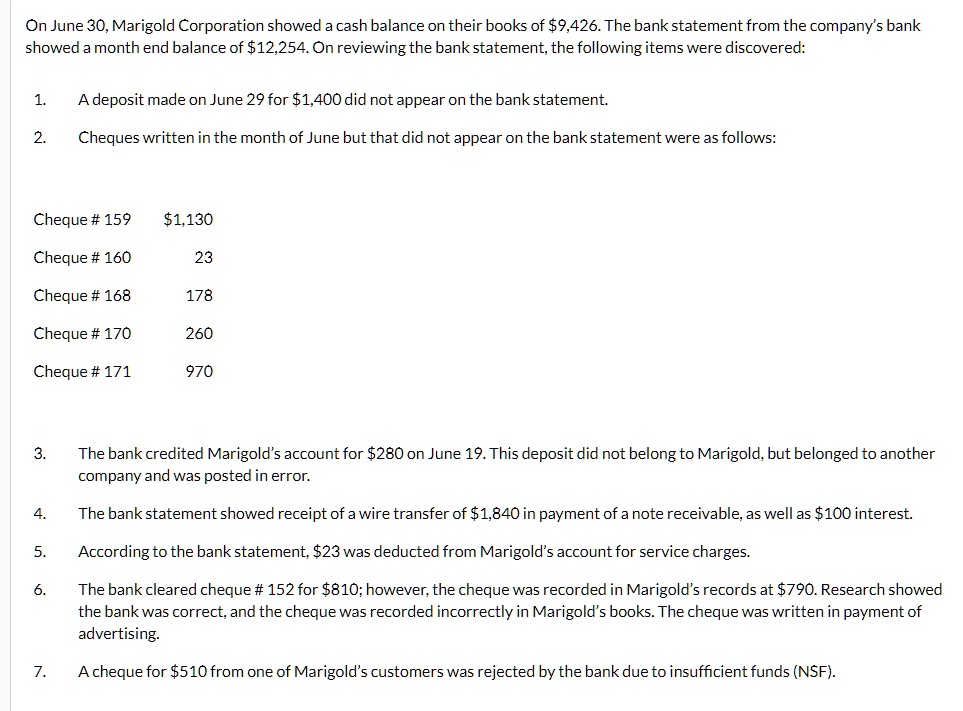

On June 30, Marigold Corporation showed a cash balance on their books of $9,426. The bank statement from the company's bank showed a month end balance of $12,254. On reviewing the bank statement, the following items were discovered:

1.

A deposit made on June 29 for $1,400 did not appear on the bank statement.

2.

Cheques written in the month of June but that did not appear on the bank statement were as follows:

Cheque # 159

$1,130

Cheque # 160

23

Cheque # 168

178

Cheque # 170

260

Cheque # 171

970

3.

The bank credited Marigold's account for $280 on June 19. This deposit did not belong to Marigold, but belonged to another company and was posted in error.

4.

The bank statement showed receipt of a wire transfer of $1,840 in payment of a note receivable, as well as $100 interest.

5.

According to the bank statement, $23 was deducted from Marigold's account for service charges.

6.

The bank cleared cheque # 152 for $810; however, the cheque was recorded in Marigold's records at $790. Research showed the bank was correct, and the cheque was recorded incorrectly in Marigold's books. The cheque was written in payment of advertising.

7.

A cheque for $510 from one of Marigold's customers was rejected by the bank due to insufficient funds (NSF).