Question 2

Dave Ltd manufactures glass for the construction industry. The company has two

production departments: Machining and Finishing. There are also two support

departments: Ordering and Design. The budgeted overhead costs for the year for each

department are as follows:

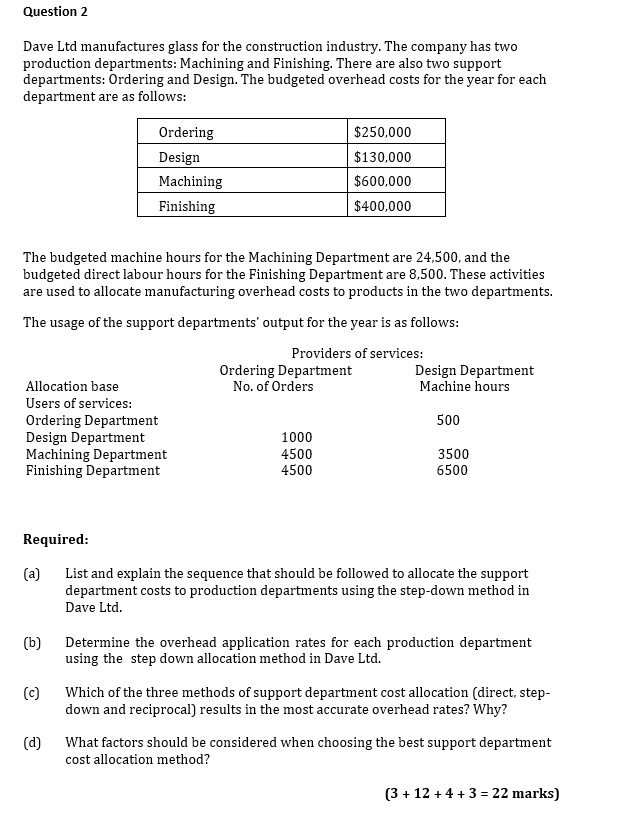

Ordering

$250,000

Design

$130,000

Machining

$600,000

Finishing

$400,000

The budgeted machine hours for the Machining Department are 24,500, and the

budgeted direct labour hours for the Finishing Department are 8,500. These activities

are used to allocate manufacturing overhead costs to products in the two departments.

The usage of the support departments' output for the year is as follows:

Providers of services:

Allocation base

Ordering Department

Design Department

No. of Orders

Machine hours

Users of services:

Ordering Department

500

Design Department

1000

Machining Department

4500

3500

Finishing Department

4500

6500

Required:

(a) List and explain the sequence that should be followed to allocate the support

department costs to production departments using the step-down method in

Dave Ltd.

(b) Determine the overhead application rates for each production department

using the step down allocation method in Dave Ltd.

(c) Which of the three methods of support department cost allocation (direct, step-

down and reciprocal) results in the most accurate overhead rates? Why?

(d) What factors should be considered when choosing the best support department

cost allocation method?

(3 + 12 + 4 + 3 = 22 marks)