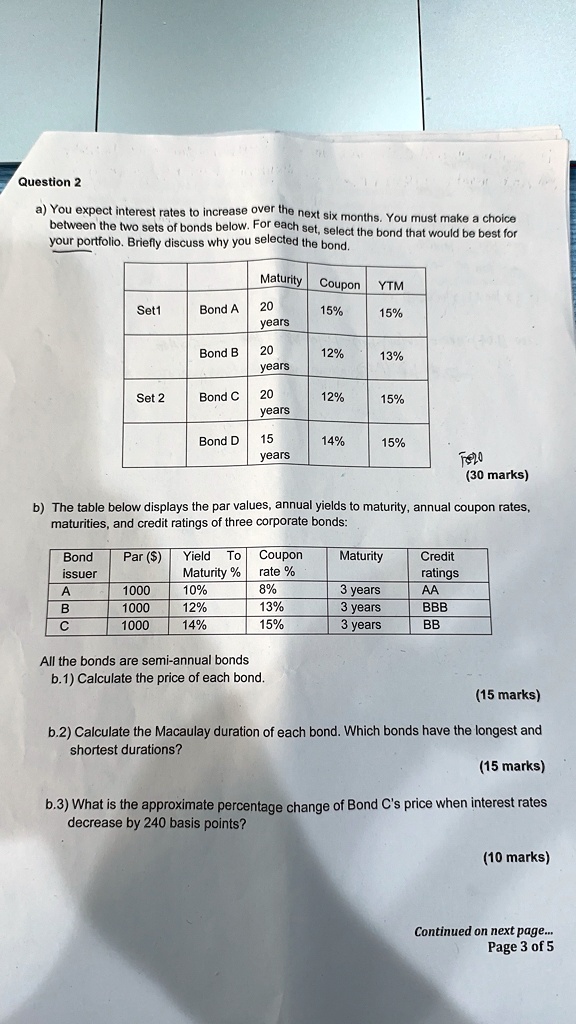

Question 2

a) You expect interest rates to increase over the next six months. You must make a choice

between the two sets of bonds below. For each set, select the bond that would be best for

your portfolio. Briefly discuss why you selected the bond.

Maturity Coupon YTM

Set1

Bond A

20

years

15%

15%

Bond B

20

12%

13%

years

Set 2

Bond C

20

12%

15%

years

Bond D

15

14%

15%

years

F20

(30 marks)

b) The table below displays the par values, annual yields to maturity, annual coupon rates,

maturities, and credit ratings of three corporate bonds:

Bond

Par ($)

Yield To

Coupon

Maturity

Credit

issuer

Maturity % rate %

ratings

A

1000

10%

8%

3 years

AA

B

1000

12%

13%

3 years

BBB

C

1000

14%

15%

3 years

BB

All the bonds are semi-annual bonds

b.1) Calculate the price of each bond.

(15 marks)

b.2) Calculate the Macaulay duration of each bond. Which bonds have the longest and

shortest durations?

(15 marks)

b.3) What is the approximate percentage change of Bond C's price when interest rates

decrease by 240 basis points?

(10 marks)

Continued on next page...

Page 3 of 5