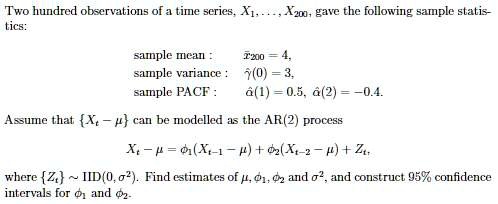

Time series" question:

Two hundred observations of a time series, X, gave the following sample statistics:

sample mean: 200.4, sample variance: 0.3, sample PACF: 1.0.5, a2 = -0.4

Assume that {X-} can be modeled as the AR(2) process

where {Z} ~ IID. Find estimates of 1 and and construct 95% confidence intervals for and.