[7 Marks]

Q 2(a)

Explain the concept of risk aversion and explain the ways in which risk aversion may

be estimated.

Q 2(b)

[18 Marks]

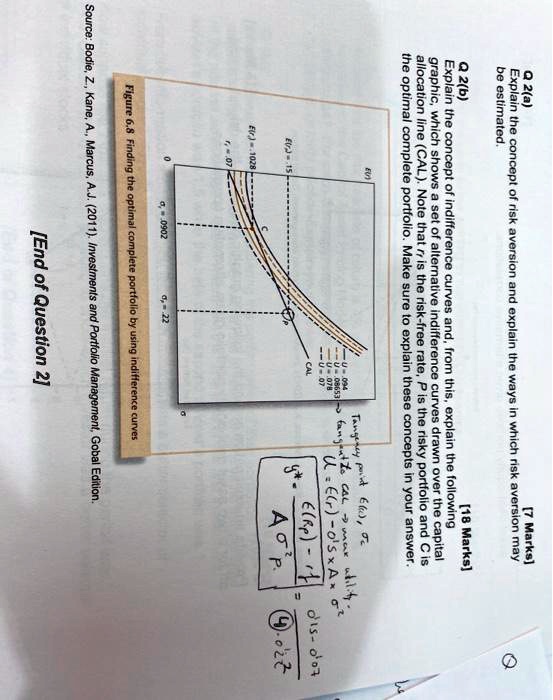

Explain the concept of indifference curves and, from this, explain the following

graphic, which shows a set of alternative indifference curves drawn over the capital

allocation line (CAL). Note that $r_f$ is the risk-free rate, P is the risky portfolio and C is

the optimal complete portfolio. Make sure to explain these concepts in your answer.

$E(r) = 15$

$E(r) = 1028$

$r_f = 0.07$

$U = 0.94$

$U = 0.8653$

$U = 0.78$

$U = 0.7$

CAL

Tangency point $\left(\bar{r}, \bar{\sigma}\right)$,

$\text{tangent to CAL max utility}$

$U = E(r) - \frac{1}{2} \times A \times \sigma^2$

$y^* = \frac{E(r_p) - r_f}{A \sigma_p^2} = \frac{0.15 - 0.07}{4 \times 0.22^2}$

$P$

$\sigma_p = 0.902$

$\sigma_p = 0.22$

Figure 6.8 Finding the optimal complete portfolio by using indifference curves

Source: Bodie, Z., Kane, A., Marcus, A.J. (2011). Investments and Portfolio Management, Gobal Edition.

[End of Question 2]