CHANGE IN PROFIT SHARING RATIO AMONG THE EXISTING PARTNERS

2.73

16 PARTive

ance

\( A ? 3,82,8 i i \)

\begin{tabular}{|c|c|c|c|c|}

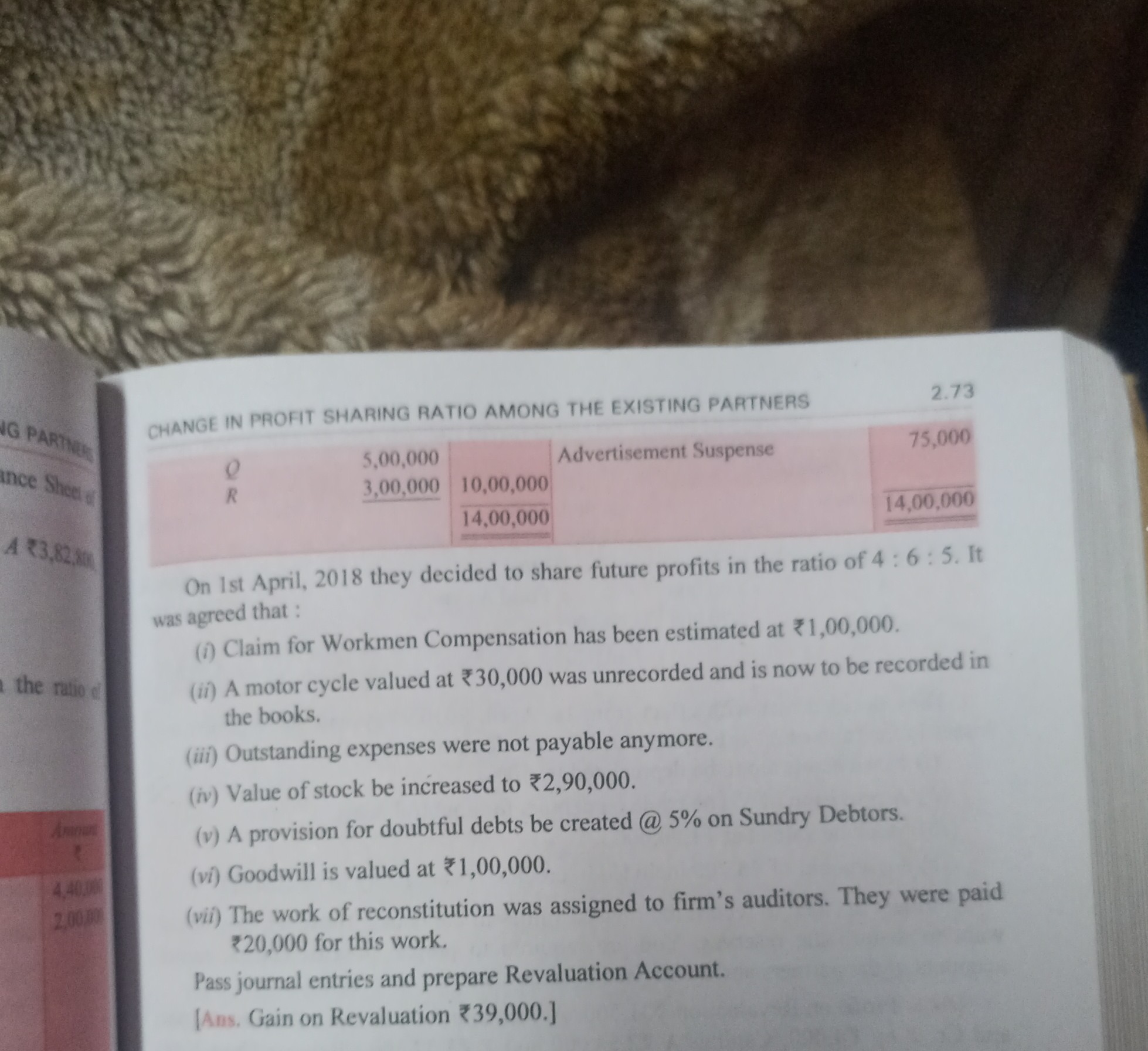

\hline 0 & \( 5,00,000 \) & & Advertisement Suspense & 75,000 \\

\hline\( R \) & \( 3,00,000 \) & \( 10,00,000 \) & & \\

\hline & & \( 14,00,000 \) & & \( 14,00,00 \) \\

\hline

\end{tabular}

On 1st April, 2018 they decided to share future profits in the ratio of \( 4: 6: 5 \). It was agreed that :

(i) Claim for Workmen Compensation has been estimated at \( ? 1,00,000 \).

(ii) A motor cycle valued at \( ? 30,000 \) was unrecorded and is now to be recorded in the books.

(iii) Outstanding expenses were not payable anymore.

(iv) Value of stock be increased to \( ? 2,90,000 \).

(v) A provision for doubtful debts be created (a) \( 5 \% \) on Sundry Debtors.

(vi) Goodwill is valued at \( ? 1,00,000 \).

(vii) The work of reconstitution was assigned to firm's auditors. They were paid \( ? 20,000 \) for this work.

Pass journal entries and prepare Revaluation Account.

[Ans, Gain on Revaluation ?39,000.]