A. For deferred taxes, why is there a negative number in the liability columns for 2023?

B. Why did this negative number change from 2022 to 2023?

C. Why are there also numbers in the asset columns for 2022 and 2023?

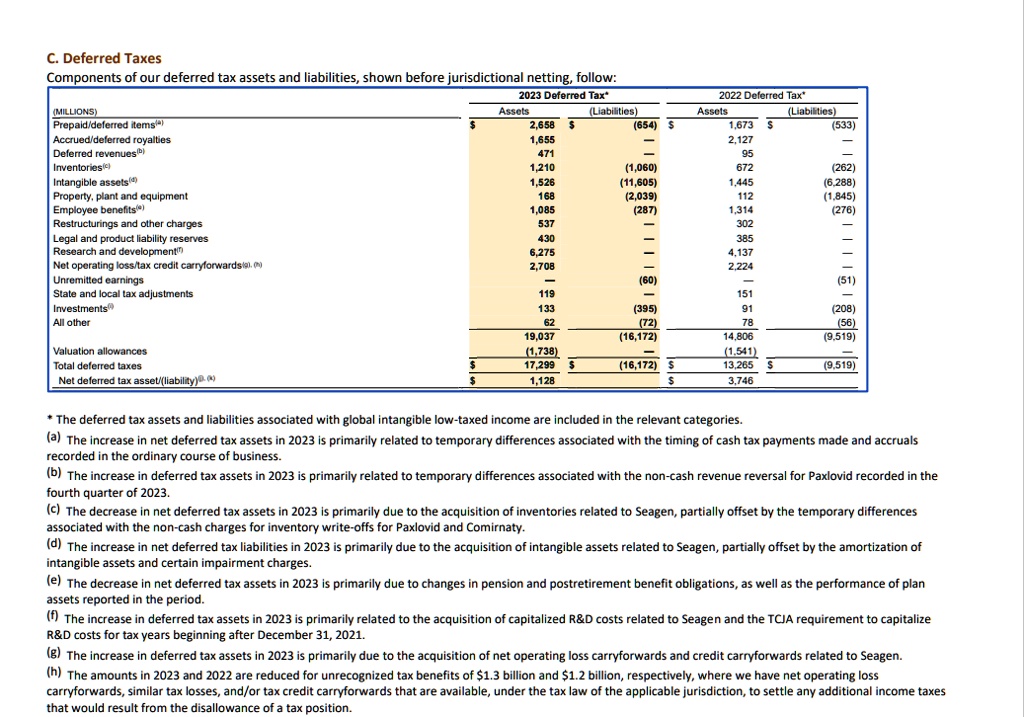

Deferred Taxes Components of our deferred tax assets and liabilities, shown before jurisdictional netting, follow:

2023 Deferred Tax* (MILLIONS) Assets (Liabilities)

Prepaid/deferred items 2,658 (654)

Accrued/deferred royalties 1,655

Deferred revenues 471

Inventories 1,210 (1,060)

Intangible assets 1,526 (11,605)

Property, plant and equipment 168 (2,039)

Employee benefits 1,085 (287)

Restructurings and other charges 537

Legal and product liability reserves 430

Research and development 6,275

Net operating loss/tax credit carryforwards 2,708

Unremitted earnings (60)

State and local tax adjustments 119

Investments 133 (42)

All other 62 (72)

19,037 (16,172)

Valuation allowances (1,738)

Total deferred taxes 17,299 (16,172)

Net deferred tax asset/(liability) 1,128

2022 Deferred Tax* Assets (Liabilities)

1,673 (533)

2,127 95

672 (262)

1,445 (6,288)

112 (1,845)

1,314 (276)

302 385

4,137 2,224

(51) 151

91 (208)

78 (56)

14,806 (9,519)

(1,541) 13,265 (9,519)

3,746

* The deferred tax assets and liabilities associated with global intangible low-taxed income are included in the relevant categories

(a) The increase in net deferred tax assets in 2023 is primarily related to temporary differences associated with the timing of cash tax payments made and accruals recorded in the ordinary course of business.

fourth quarter of 2023.

(c) The decrease in net deferred tax assets in 2023 is primarily due to the acquisition of inventories related to Seagen, partially offset by the temporary differences in intangible assets and certain impairment charges.

(e) The decrease in net deferred tax assets in 2023 is primarily due to changes in pension and postretirement benefit obligations, as well as the performance of plan assets reported in the period.

(f) The increase in deferred tax assets in 2023 is primarily related to the acquisition of capitalized R&D costs related to Seagen and the TCJA requirement to capitalize R&D costs for tax years beginning after December 31, 2021.

(g) The increase in deferred tax assets in 2023 is primarily due to the acquisition of net operating loss carryforwards and credit carryforwards related to Seagen.

carryforwards, similar tax losses, and/or tax credit carryforwards that are available, under the tax law of the applicable jurisdiction, to settle any additional income taxes that would result from the disallowance of a tax position.