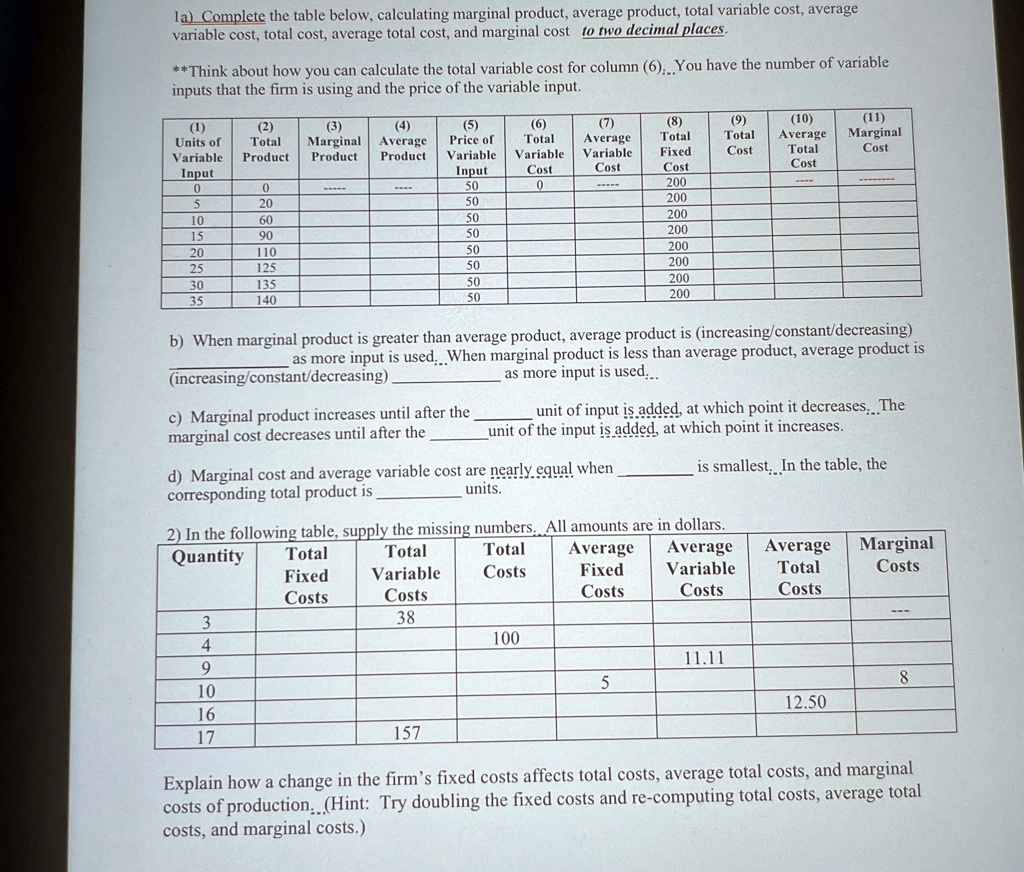

1a) Complete the table below, calculating marginal product, average product, total variable cost, average

variable cost, total cost, average total cost, and marginal cost to two decimal places.

**Think about how you can calculate the total variable cost for column (6). You have the number of variable

inputs that the firm is using and the price of the variable input.

(3)

(4)

Marginal Average

Product Product

(1)

Units of

Variable

(2)

Total

Product

Input

0

0

5

20

10

60

15

90

20

110

25

125

30

135

35

140

(5)

Price of

Variable

(6)

(7)

(8)

(9)

(10)

(11)

Total

Average

Total

Total

Average

Marginal

Variable Variable

Fixed

Cost

Total

Cost

Input

Cost

Cost

Cost

Cost

50

0

200

50

200

50

200

50

200

50

200

50

200

50

200

50

200

b) When marginal product is greater than average product, average product is (increasing/constant/decreasing)

as more input is used. When marginal product is less than average product, average product is

(increasing/constant/decreasing)

as more input is used...

c) Marginal product increases until after the

unit of input is added, at which point it decreases. The

marginal cost decreases until after the

unit of the input is added, at which point it increases.

d) Marginal cost and average variable cost are nearly equal when

corresponding total product is

is smallest. In the table, the

units.

2) In the following table, supply the missing numbers. All amounts are in dollars.

Quantity

Total

Total

Fixed

Variable

Total

Costs

Average Average Average Marginal

Costs

Costs

Fixed

Costs

Variable

Total

Costs

Costs

Costs

3

38

4

100

11.11

9

10

5

8

12.50

16

17

157

Explain how a change in the firm's fixed costs affects total costs, average total costs, and marginal

costs of production. (Hint: Try doubling the fixed costs and re-computing total costs, average total

costs, and marginal costs.)