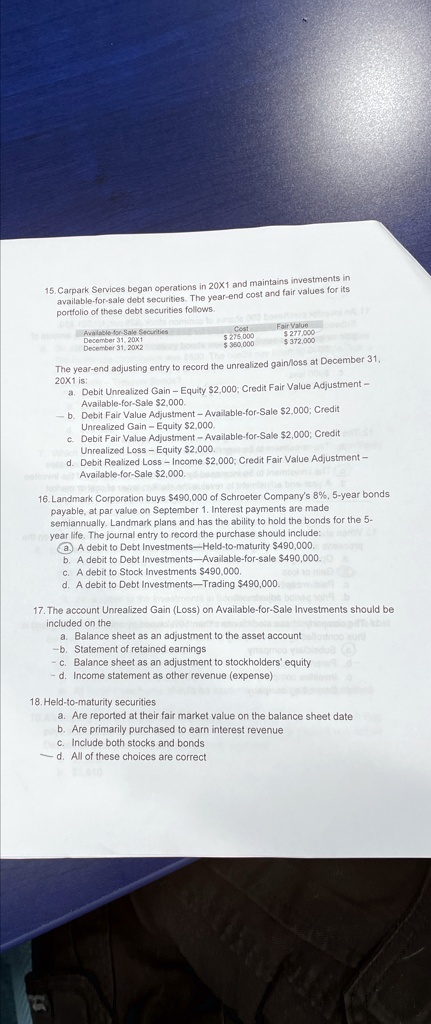

15. Carpark Services began operations in 20X1 and maintains investments in

available-for-sale debt securities. The year-end cost and fair values for its

portfolio of these debt securities follows.

Available-for-Sale Securities

December 31, 20X1

December 31, 20X2

Cost

Fair Value

$ 275,000

$ 360,000

$ 277,000

$ 372,000

The year-end adjusting entry to record the unrealized gain/loss at December 31,

20X1 is:

a. Debit Unrealized Gain - Equity $2,000; Credit Fair Value Adjustment -

Available-for-Sale $2,000.

b. Debit Fair Value Adjustment - Available-for-Sale $2,000; Credit

Unrealized Gain - Equity $2,000.

c. Debit Fair Value Adjustment - Available-for-Sale $2,000; Credit

Unrealized Loss - Equity $2,000.

d. Debit Realized Loss - Income $2,000; Credit Fair Value Adjustment -

Available-for-Sale $2,000.

16. Landmark Corporation buys $490,000 of Schroeter Company's 8%, 5-year bonds

payable, at par value on September 1. Interest payments are made

semiannually. Landmark plans and has the ability to hold the bonds for the 5-

year life. The journal entry to record the purchase should include:

a. A debit to Debt Investments-Held-to-maturity $490,000.

b. A debit to Debt Investments-Available-for-sale $490,000.

c. A debit to Stock Investments $490,000.

d. A debit to Debt Investments-Trading $490,000.

17. The account Unrealized Gain (Loss) on Available-for-Sale Investments should be

included on the

a. Balance sheet as an adjustment to the asset account

b. Statement of retained earnings

c. Balance sheet as an adjustment to stockholders' equity

d. Income statement as other revenue (expense)

18. Held-to-maturity securities

a. Are reported at their fair market value on the balance sheet date

b. Are primarily purchased to earn interest revenue

c. Include both stocks and bonds

d. All of these choices are correct