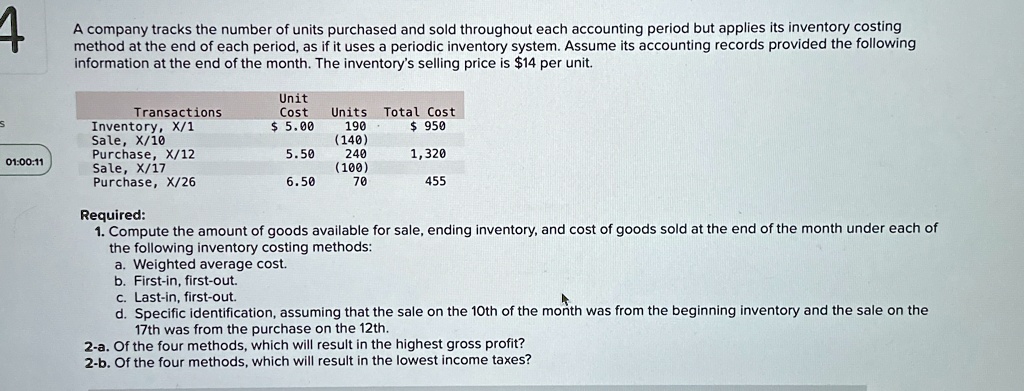

A company tracks the number of units purchased and sold throughout each accounting period but applies its inventory costing method at the end of each period, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the month. The inventory's selling price is $14 per unit.

Unit

Transactions

Cost

Units

Total Cost

Inventory, X/1

$ 5.00

190

$ 950

Sale, X/10

(140)

Purchase, X/12

5.50

240

1,320

Sale, X/17

(100)

Purchase, X/26

6.50

70

455

Required:

1. Compute the amount of goods available for sale, ending inventory, and cost of goods sold at the end of the month under each of the following inventory costing methods:

a. Weighted average cost.

b. First-in, first-out.

c. Last-in, first-out.

d. Specific identification, assuming that the sale on the 10th of the month was from the beginning inventory and the sale on the 17th was from the purchase on the 12th.

2-a. Of the four methods, which will result in the highest gross profit?

2-b. Of the four methods, which will result in the lowest income taxes?