Fund Types

The transactions of the authority are accounted for in the following governmental fund types:

• General fund—To account for all revenues and expenditures not required to be accounted for in other funds.

• Capital projects fund—To account for and report financial resources that are restricted, committed, or

assigned to expenditure for capital outlays. Such resources are derived principally from other municipal

utility districts to which the Williamsburg Regional Sewage Treatment Authority provides certain services.

1. Recast the balance sheets of the two funds into a single consolidated balance sheet (statement of net

position). Show separately, however, the restricted and the unrestricted portions of the consolidated net

position (not each individual asset and liability). Be sure to eliminate interfund payables and receivables.

2. Which presentation, the unconsolidated or the consolidated, provides more complete information?

Explain. Which presentation might be seen as misleading? Why? What, if any, advantages do you see

in this presentation even though it might be less complete and more misleading?

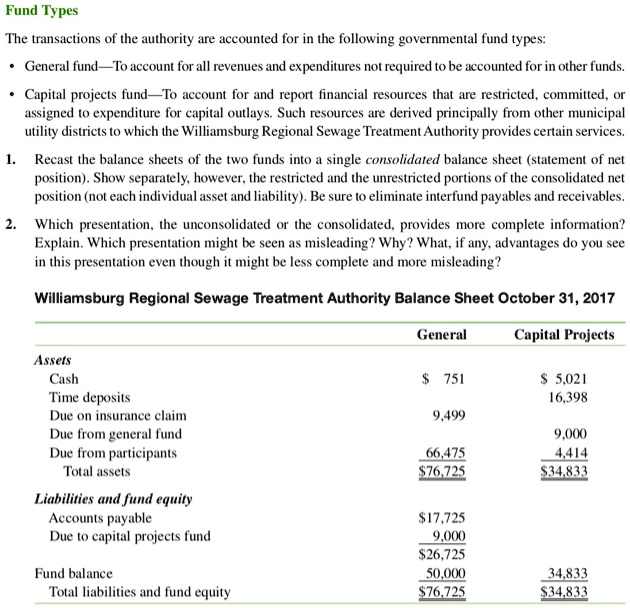

Williamsburg Regional Sewage Treatment Authority Balance Sheet October 31, 2017

General

Capital Projects

Assets

Cash

$ 751

$ 5,021

Time deposits

16,398

Due on insurance claim

9,499

Due from general fund

9,000

Due from participants

66,475

4,414

Total assets

$76,725

$34,833

Liabilities and fund equity

Accounts payable

$17,725

Due to capital projects fund

9,000

$26,725

Fund balance

50,000

34,833

Total liabilities and fund equity

$76,725

$34,833