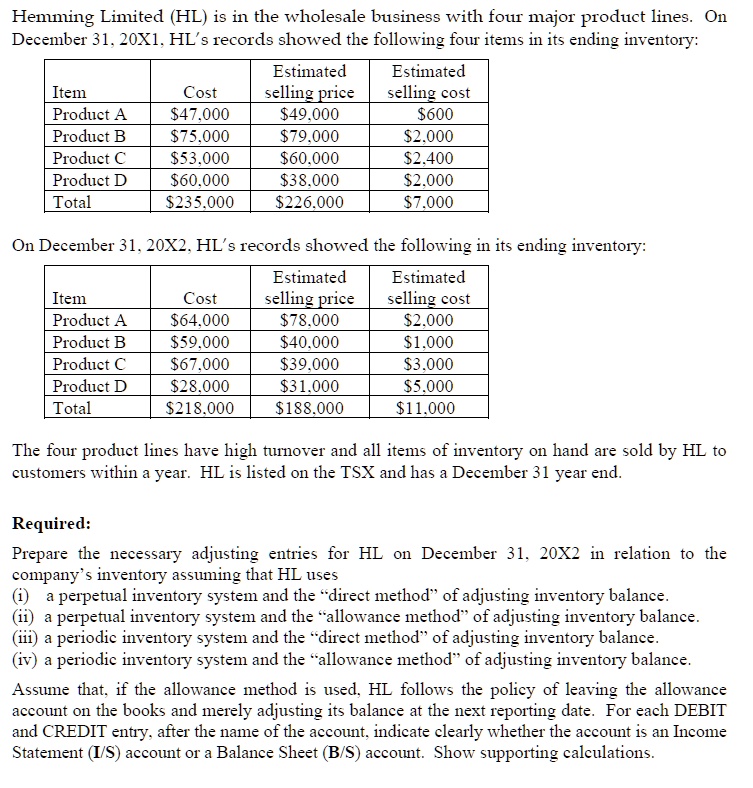

Hemming Limited (HL) is in the wholesale business with four major product lines. On December 31, 20X1, HL's records showed the following four items in its ending inventory:

Estimated selling price: $49,000, $79,000, $60,000, $38,000

Estimated selling cost: $600, $2,000, $2,400, $2,000

Item: Product A, Product B, Product C, Product D

Cost: $47,000, $75,000, $53,000, $60,000

Total cost: $235,000

On December 31, 20X2, HL's records showed the following in its ending inventory:

Estimated selling price: $78,000, $40,000, $39,000, $31,000

Estimated selling cost: $2,000, $1,000, $3,000, $5,000

Item: Product A, Product B, Product C, Product D

Cost: $64,000, $59,000, $67,000, $28,000

Total cost: $218,000

The four product lines have high turnover, and all items of inventory on hand are sold by HL to customers within a year. HL is listed on the TSX and has a December 31 year-end.

Required:

Prepare the necessary adjusting entries for HL on December 31, 20X2, in relation to the company's inventory, assuming that HL uses:

(i) a perpetual inventory system and the "direct method" of adjusting inventory balance.

(ii) a perpetual inventory system and the "allowance method" of adjusting inventory balance.

(iii) a periodic inventory system and the "direct method" of adjusting inventory balance.

(iv) a periodic inventory system and the allowance method of adjusting inventory balance.

Assume that if the allowance method is used, HL follows the policy of leaving the allowance account on the books and merely adjusting its balance at the next reporting date. For each DEBIT and CREDIT entry, after the name of the account, indicate clearly whether the account is an Income Statement (I/S) account or a Balance Sheet (B/S) account. Show supporting calculations.