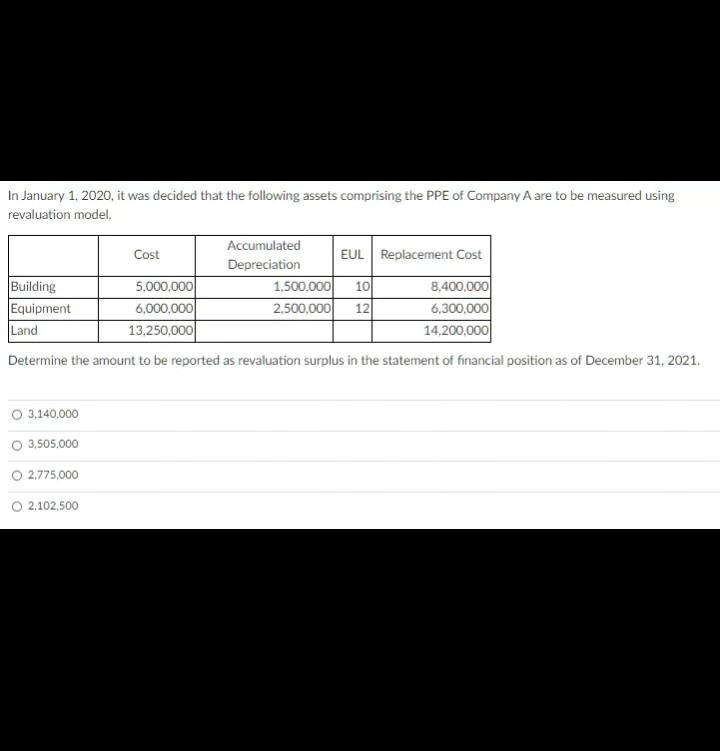

In January 1, 2020, it was decided that the following assets comprising the PPE of Company A are to be measured using

revaluation model.

Building

Equipment

Land

Accumulated

Cost

EUL Replacement Cost

Depreciation

5,000,000

1,500,000

10

8,400,000

6,000,000

2,500,000

12

6,300,000

13,250,000

14,200,000

Determine the amount to be reported as revaluation surplus in the statement of financial position as of December 31, 2021.

? 3,140,000

? 3,505,000

? 2,775,000

? 2,102,500