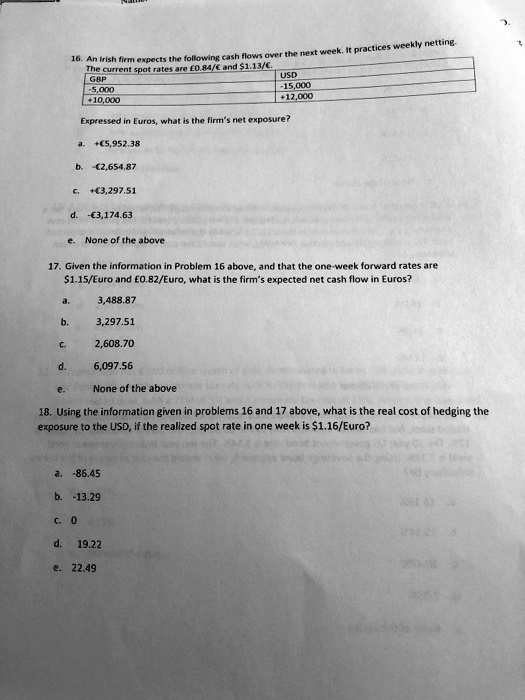

16. An Irish firm expects the following cash flows over the next week. It practices weekly netting.

The current spot rates are £0.84/€ and $1.13/€.

GBP

-5,000

+10,000

USD

-15,000

+12,000

Expressed in Euros, what is the firm's net exposure?

a. +€5,952.38

b. -€2,654.87

c. +€3,297.51

d. -€3,174.63

e. None of the above

17. Given the information in Problem 16 above, and that the one-week forward rates are

$1.15/Euro and £0.82/Euro, what is the firm's expected net cash flow in Euros?

a.

3,488.87

b.

3,297.51

c.

2,608.70

d.

6,097.56

e.

None of the above

18. Using the information given in problems 16 and 17 above, what is the real cost of hedging the

exposure to the USD, if the realized spot rate in one week is $1.16/Euro?

a. -86.45

b. -13.29

c. 0

d. 19.22

e. 22.49