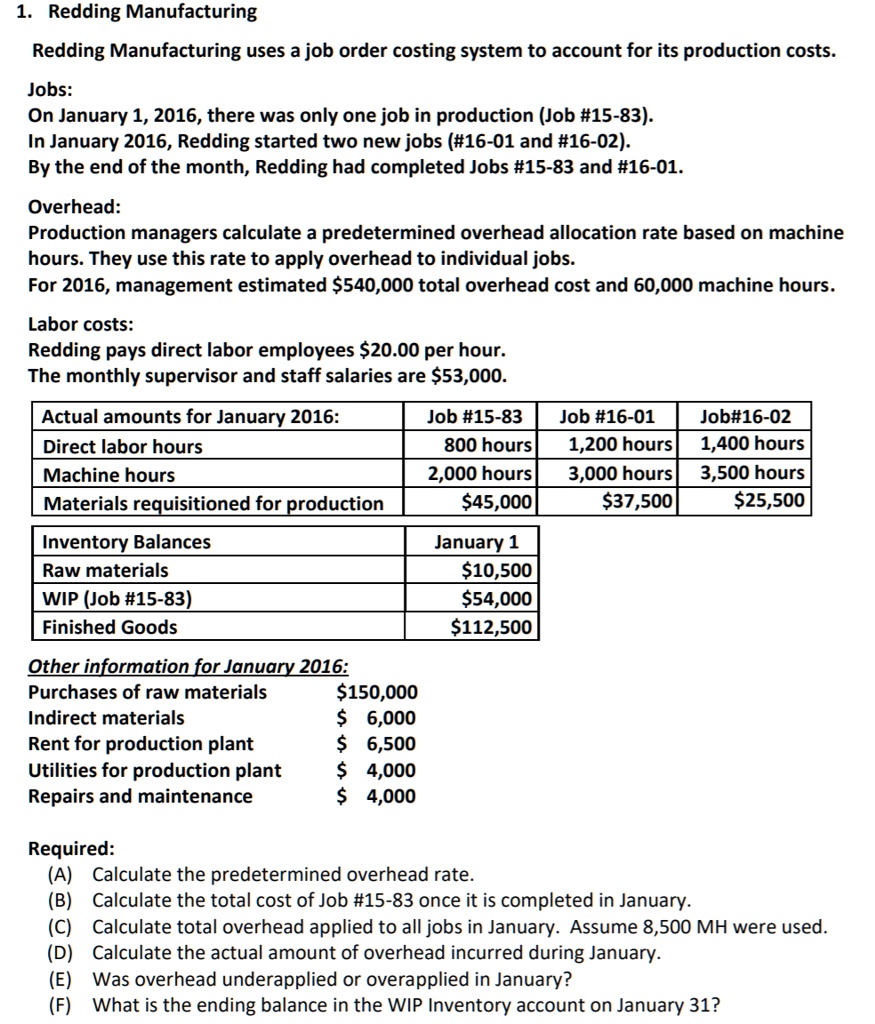

Redding Manufacturing uses a job order costing system to account for its production costs.

Jobs: On January 1, 2016, there was only one job in production (Job #15-83). In January 2016, Redding started two new jobs (#16-01 and #16-02). By the end of the month, Redding had completed Jobs #15-83 and #16-01.

Overhead: Production managers calculate a predetermined overhead allocation rate based on machine hours. They use this rate to apply overhead to individual jobs. For 2016, management estimated $540,000 total overhead cost and 60,000 machine hours.

Labor costs: Redding pays direct labor employees $20.00 per hour. The monthly supervisor and staff salaries are $53,000.

Actual amounts for January 2016:

Job #15-83: 800 hours, 2,000 machine hours, $45,000

Job #16-01: 1,200 hours, 3,000 machine hours, $37,500

Job #16-02: 1,400 hours, 3,500 machine hours, $25,500

Direct labor hours: 8,500

Machine hours: 60,000

Materials requisitioned for production:

January 1:

Raw materials: $10,500

Work in progress (Job #15-83): $54,000

Finished Goods: $112,500

Other information for January 2016:

Purchases of raw materials: $150,000

Indirect materials: $6,000

Rent for production plant: $6,500

Utilities for production plant: $4,000

Repairs and maintenance: $4,000

Required:

(A) Calculate the predetermined overhead rate.

(B) Calculate the total cost of Job #15-83 once it is completed in January.

(C) Calculate total overhead applied to all jobs in January. Assume 8,500 machine hours were used.

(D) Calculate the actual amount of overhead incurred during January.

(E) Was overhead underapplied or overapplied in January?

(F) What is the ending balance in the Work in Progress (WIP) Inventory account on January 31?