Your answer is correct.

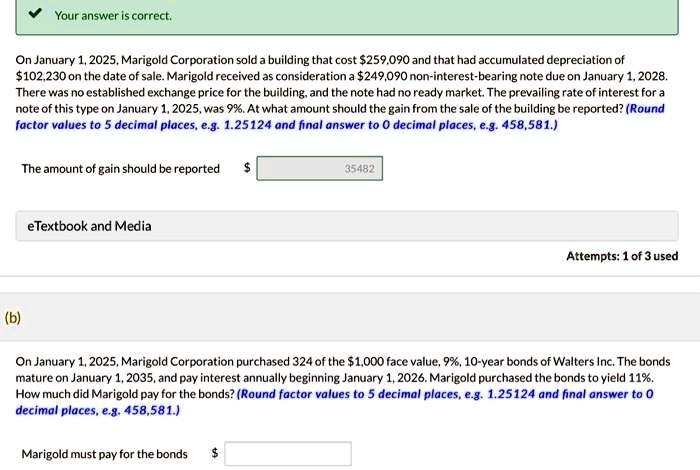

On January 1, 2025, Marigold Corporation sold a building that cost $259,090 and that had accumulated depreciation of

$102,230 on the date of sale. Marigold received as consideration a $249,090 non-interest-bearing note due on January 1, 2028.

There was no established exchange price for the building, and the note had no ready market. The prevailing rate of interest for a

note of this type on January 1, 2025, was 9%. At what amount should the gain from the sale of the building be reported? (Round

factor values to 5 decimal places, e.g. 1.25124 and final answer to O decimal places, e.g. 458,581.)

The amount of gain should be reported

$

35482

eTextbook and Media

Attempts: 1 of 3 used

(b)

On January 1, 2025, Marigold Corporation purchased 324 of the $1,000 face value, 9%, 10-year bonds of Walters Inc. The bonds

mature on January 1, 2035, and pay interest annually beginning January 1, 2026. Marigold purchased the bonds to yield 11%.

How much did Marigold pay for the bonds? (Round factor values to 5 decimal places, e.g. 1.25124 and final answer to 0

decimal places, e.g. 458,581.)

Marigold must pay for the bonds

$