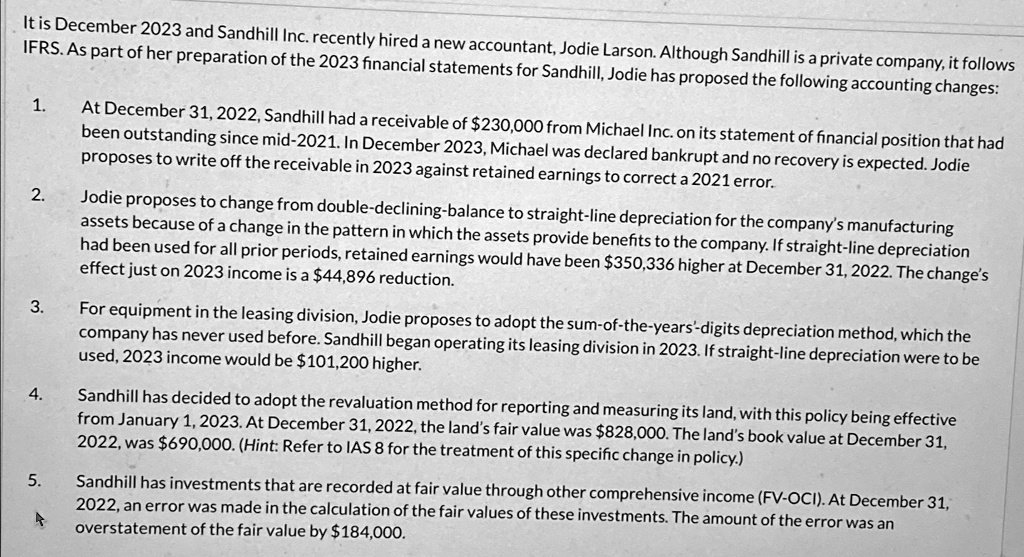

It is December 2023 and Sandhill Inc. recently hired a new accountant, Jodie Larson. Although Sandhill is a private company, it follows IFRS. As part of her preparation of the 2023 financial statements for Sandhill, Jodie has proposed the following accounting changes:

At December 31,2022 , Sandhill had a receivable of $230,000 from Michael Inc. on its statement of financial position that had been outstanding since mid-2021. In December 2023, Michael was declared bankrupt and no recovery is expected. Jodie proposes to write off the receivable in 2023 against retained earnings to correct a 2021 error.

Jodie proposes to change from double-declining-balance to straight-line depreciation for the company's manufacturing assets because of a change in the pattern in which the assets provide benefits to the company. If straight-line depreciation had been used for all prior periods, retained earnings would have been $350,336 higher at December 31,2022 . The change's effect just on 2023 income is a $44,896 reduction.

For equipment in the leasing division, Jodie proposes to adopt the sum-of-the-years'-digits depreciation method, which the company has never used before. Sandhill began operating its leasing division in 2023. If straight-line depreciation were to be used, 2023 income would be $101,200 higher.

Sandhill has decided to adopt the revaluation method for reporting and measuring its land, with this policy being effective from January 1, 2023. At December 31, 2022, the land's fair value was $828,000. The land's book value at December 31 , 2022 , was $690,000. (Hint: Refer to IAS 8 for the treatment of this specific change in policy.)

Sandhill has investments that are recorded at fair value through other comprehensive income (FV-OCI). At December 31, 2022, an error was made in the calculation of the fair values of these investments. The amount of the error was an overstatement of the fair value by $184,000.

Prepare the required journal entries to record any adjustments.

Please

Do the journal entries

It is December 2023 and Sandhill Inc. recently hired a new accountant, Jodie Larson. Although Sandhill is a private company, it follows IFRS. As part of her preparation of the 2023 financial statements for Sandhill, Jodie has proposed the following accounting changes: 1. At December 31, 2022, Sandhill had a receivable of $230,000 from Michael Inc. on its statement of financial position that had been outstanding since mid-2021.In December 2023,Michael was declared bankrupt and no recovery is expected.Jodie proposes to write off the receivable in 2023 against retained earnings to correct a 2021 error. 2. Jodie proposes to change from double-declining-balance to straight-line depreciation for the company's manufacturing assets because of a change in the pattern in which the assets provide benefits to the company.If straight-line depreciation effect just on 2023 income is a$44,896reduction. had been used for all prior periods,retained earnings would have been $350,336 higher at December 31,2022.The change's 3. For eguipment in the leasing division, Jodie proposes to adopt the sum-of-the-years'-digits depreciation method,which the used,2023 income would be$101,200 higher. company has never used before.Sandhill began operating its leasing division in 2023.If straight-line depreciation were to be 4. Sandhill has decided to adopt the revaluation method for reporting and measuring its land,with this policy being effective from January 1, 2023. At December 31, 2022, the land's fair value was $828,000. The land's book value at December 31, 2022,was$690,000.(Hint:Refer to IAS8 for the treatment of this specific change in policy.) 5. Sandhill has investments that are recorded at fair value through other comprehensive income (FV-OCI). At December 31, A 2022, an error was made in the calculation of the fair values of these investments. The amount of the error was an overstatement of the fair value by$184,000