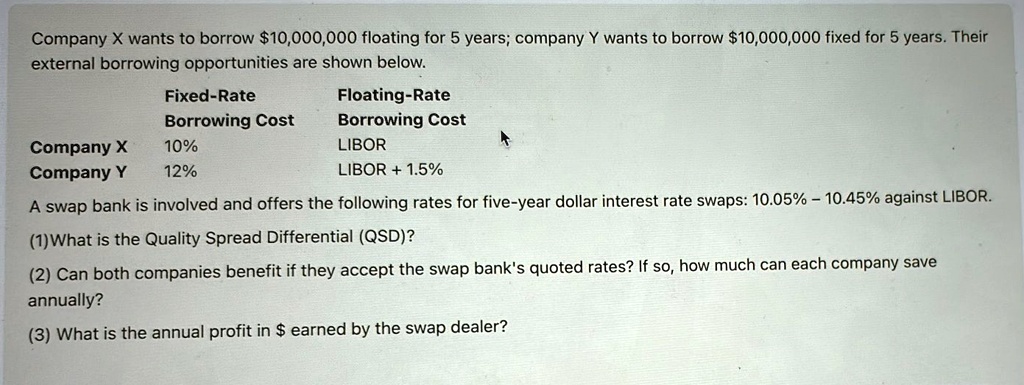

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their

external borrowing opportunities are shown below.

Fixed-Rate

Floating-Rate

Borrowing Cost

Borrowing Cost

Company X

10%

LIBOR

Company Y

12%

LIBOR + 1.5%

A swap bank is involved and offers the following rates for five-year dollar interest rate swaps: 10.05% - 10.45% against LIBOR.

(1) What is the Quality Spread Differential (QSD)?

(2) Can both companies benefit if they accept the swap bank's quoted rates? If so, how much can each company save

annually?

(3) What is the annual profit in $ earned by the swap dealer?