8. Consider the model

$y = \alpha + \beta_1 x_1 + \beta_2 x_2 + \epsilon$

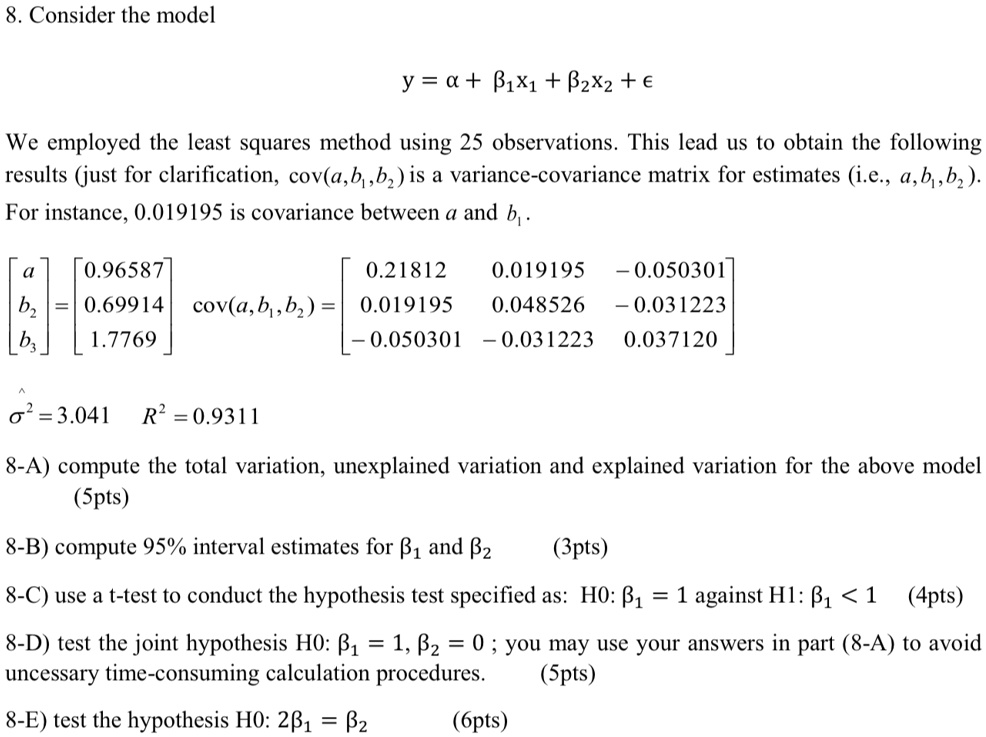

We employed the least squares method using 25 observations. This lead us to obtain the following

results (just for clarification, $cov(a, b_1, b_2)$ is a variance-covariance matrix for estimates (i.e., $a, b_1, b_2$).

For instance, 0.019195 is covariance between a and $b_1$.

$\begin{bmatrix} a \\ b_1 \\ b_2 \end{bmatrix} = \begin{bmatrix} 0.96587 \\ 0.69914 \\ 1.7769 \end{bmatrix}$

$cov(a, b_1, b_2) = \begin{bmatrix} 0.21812 & 0.019195 & -0.050301 \\ 0.019195 & 0.048526 & -0.031223 \\ -0.050301 & -0.031223 & 0.037120 \end{bmatrix}$

$\hat{\sigma}^2 = 3.041$ $R^2 = 0.9311$

8-A) compute the total variation, unexplained variation and explained variation for the above model

(5pts)

8-B) compute 95% interval estimates for $\beta_1$ and $\beta_2$

(3pts)

8-C) use a t-test to conduct the hypothesis test specified as: H0: $\beta_1 = 1$ against H1: $\beta_1 < 1$ (4pts)

8-D) test the joint hypothesis H0: $\beta_1 = 1, \beta_2 = 0$; you may use your answers in part (8-A) to avoid

uncessary time-consuming calculation procedures.

(5pts)

8-E) test the hypothesis H0: $2\beta_1 = \beta_2$

(6pts)