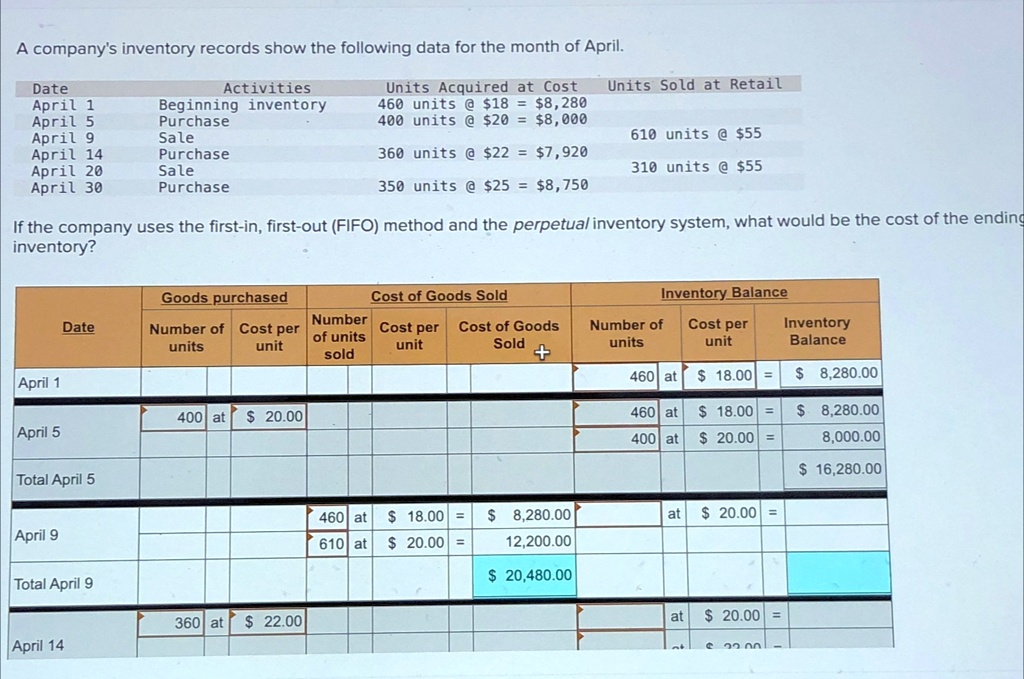

A company's inventory records show the following data for the month of April.

Date

April 1

Activities

Beginning inventory

April 5

Purchase

Units Acquired at Cost

460 units @ $18 = $8,280

400 units @ $20 = $8,000

Units Sold at Retail

April 9

Sale

610 units @ $55

April 14

Purchase

360 units @ $22 = $7,920

April 20

Sale

310 units @ $55

April 30

Purchase

350 units @ $25 = $8,750

If the company uses the first-in, first-out (FIFO) method and the perpetual inventory system, what would be the cost of the ending

inventory?

Goods purchased

Cost of Goods Sold

Inventory Balance

Date

Number of Cost per

units

unit

Number

of units

sold

Cost per

unit

Cost of Goods

Sold

+

Number of

units

Cost per

unit

Inventory

Balance

460 at

April 1

400 at $ 20.00

April 5

Total April 5

April 9

Total April 9

360 at $ 22.00

April 14

460 at

$ 18.00

610 at

$ 20.00 =

$ 8,280.00

12,200.00

$ 20,480.00

$ 18.00 =

460 at $ 18.00 =

$ 20.00 =

400 at

$ 8,280.00

$ 8,280.00

8,000.00

$ 16,280.00

at

$ 20.00 =

at

$ 20.00 =