Background

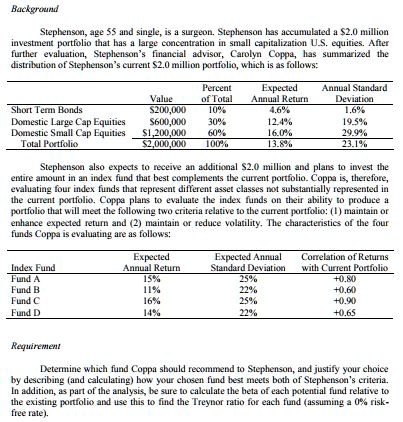

Stephenson, age 55 and single, is a surgeon. Stephenson has accumulated a $2.0 million

investment portfolio that has a large concentration in small capitalization U.S. equities. After

further evaluation, Stephenson's financial advisor, Carolyn Coppa, has summarized the

distribution of Stephenson's current $2.0 million portfolio, which is as follows:

Percent

Expected

Value

of Total

Annual Return

Annual Standard

Deviation

Short Term Bonds

$200,000

10%

4.6%

1.6%

Domestic Large Cap Equities

$600,000

30%

12.4%

19.5%

Domestic Small Cap Equities

$1,200,000

60%

16.0%

29.9%

Total Portfolio

$2,000,000

100%

13.8%

23.1%

Stephenson also expects to receive an additional $2.0 million and plans to invest the

entire amount in an index fund that best complements the current portfolio. Coppa is, therefore,

evaluating four index funds that represent different asset classes not substantially represented in

the current portfolio. Coppa plans to evaluate the index funds on their ability to produce a

portfolio that will meet the following two criteria relative to the current portfolio: (1) maintain or

enhance expected return and (2) maintain or reduce volatility. The characteristics of the four

funds Coppa is evaluating are as follows:

Index Fund

Expected

Expected Annual

Correlation of Returns

Annual Return

Standard Deviation

with Current Portfolio

Fund A

15%

25%

+0.80

Fund B

11%

22%

+0.60

Fund C

16%

25%

+0.90

Fund D

14%

22%

+0.65

Requirement

Determine which fund Coppa should recommend to Stephenson, and justify your choice

by describing (and calculating) how your chosen fund best meets both of Stephenson's criteria.

In addition, as part of the analysis, be sure to calculate the beta of each potential fund relative to

the existing portfolio and use this to find the Treynor ratio for each fund (assuming a 0% risk-

free rate).