Question 1

Ms Anita, (non-Malaysian citizen) an oil and gas engineering executive, bought a bungalow

in Cyberjaya from Mr. Kassim, for a consideration of RM 450,000. The Sales and Purchase

Agreement was signed on 1 December 2018. The bungalow was effectively transferred to her

on 1 March 2019 when the loan from the bank to finance the purchase was released to Mr.

Kassim.

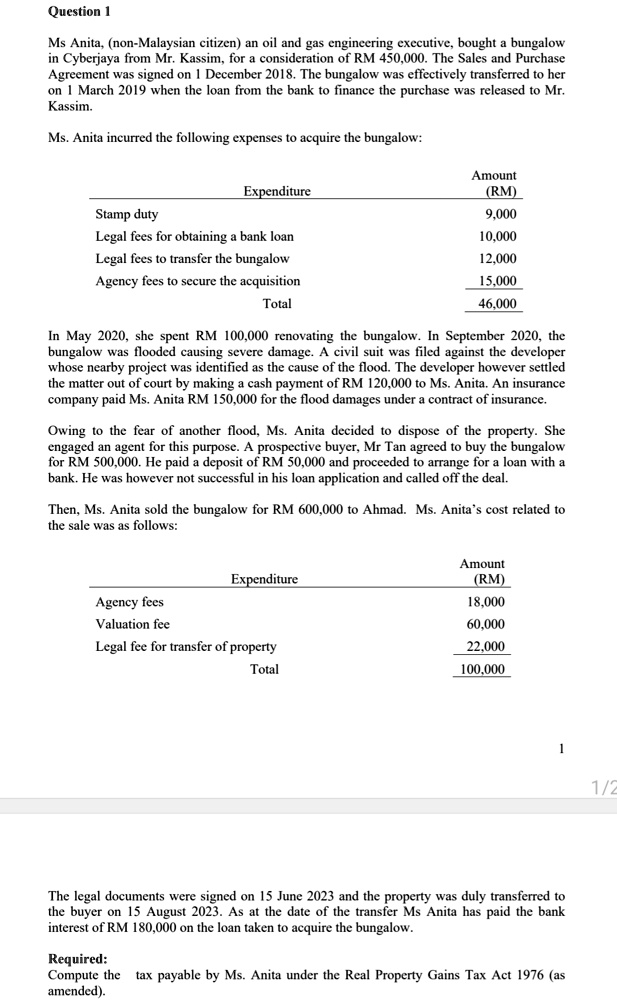

Ms. Anita incurred the following expenses to acquire the bungalow:

Stamp duty

Expenditure

Legal fees for obtaining a bank loan

Legal fees to transfer the bungalow

Agency fees to secure the acquisition

Total

Amount

(RM)

9,000

10,000

12,000

15,000

46,000

In May 2020, she spent RM 100,000 renovating the bungalow. In September 2020, the

bungalow was flooded causing severe damage. A civil suit was filed against the developer

whose nearby project was identified as the cause of the flood. The developer however settled

the matter out of court by making a cash payment of RM 120,000 to Ms. Anita. An insurance

company paid Ms. Anita RM 150,000 for the flood damages under a contract of insurance.

Owing to the fear of another flood, Ms. Anita decided to dispose of the property. She

engaged an agent for this purpose. A prospective buyer, Mr Tan agreed to buy the bungalow

for RM 500,000. He paid a deposit of RM 50,000 and proceeded to arrange for a loan with a

bank. He was however not successful in his loan application and called off the deal.

Then, Ms. Anita sold the bungalow for RM 600,000 to Ahmad. Ms. Anita's cost related to

the sale was as follows:

Agency fees

Valuation fee

Expenditure

Legal fee for transfer of property

Amount

(RM)

18,000

60,000

22,000

Total

100,000

The legal documents were signed on 15 June 2023 and the property was duly transferred to

the buyer on 15 August 2023. As at the date of the transfer Ms Anita has paid the bank

interest of RM 180,000 on the loan taken to acquire the bungalow.

Required:

Compute the tax payable by Ms. Anita under the Real Property Gains Tax Act 1976 (as

amended).

1/2