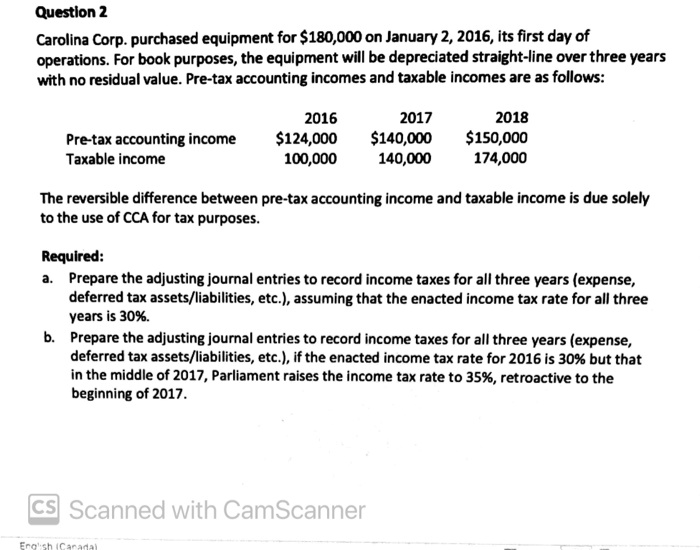

Question 2

Carolina Corp. purchased equipment for $180,000 on January 2, 2016, its first day of

operations. For book purposes, the equipment will be depreciated straight-line over three years

with no residual value. Pre-tax accounting incomes and taxable incomes are as follows:

2016

2017

2018

Pre-tax accounting income

$124,000

$140,000

$150,000

Taxable income

100,000

140,000

174,000

The reversible difference between pre-tax accounting income and taxable income is due solely

to the use of CCA for tax purposes.

Required:

a. Prepare the adjusting journal entries to record income taxes for all three years (expense,

deferred tax assets/liabilities, etc.), assuming that the enacted income tax rate for all three

years is 30%.

b. Prepare the adjusting journal entries to record income taxes for all three years (expense,

deferred tax assets/liabilities, etc.), if the enacted income tax rate for 2016 is 30% but that

in the middle of 2017, Parliament raises the income tax rate to 35%, retroactive to the

beginning of 2017.