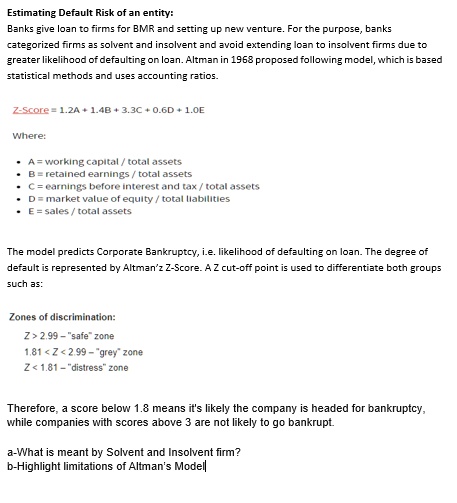

Estimating Default Risk of an entity:

Banks give loan to firms for BMR and setting up new venture. For the purpose, banks

categorized firms as solvent and insolvent and avoid extending loan to insolvent firms due to

greater likelihood of defaulting on loan. Altman in 1968 proposed following model, which is based

statistical methods and uses accounting ratios.

Z-Score = 1.2A + 1.4B + 3.3C + 0.6D + 1.0E

Where:

• A = working capital / total assets

• B = retained earnings / total assets

• C = earnings before interest and tax / total assets

• D = market value of equity / total liabilities

• E = sales / total assets

The model predicts Corporate Bankruptcy, i.e. likelihood of defaulting on loan. The degree of

default is represented by Altman'z Z-Score. A Z cut-off point is used to differentiate both groups

such as:

Zones of discrimination:

Z > 2.99 - \"safe\" zone

1.81 < Z < 2.99 - \"grey\" zone

Z < 1.81 - \"distress\" zone

Therefore, a score below 1.8 means it's likely the company is headed for bankruptcy,

while companies with scores above 3 are not likely to go bankrupt.

a-What is meant by Solvent and Insolvent firm?

b-Highlight limitations of Altman's Model