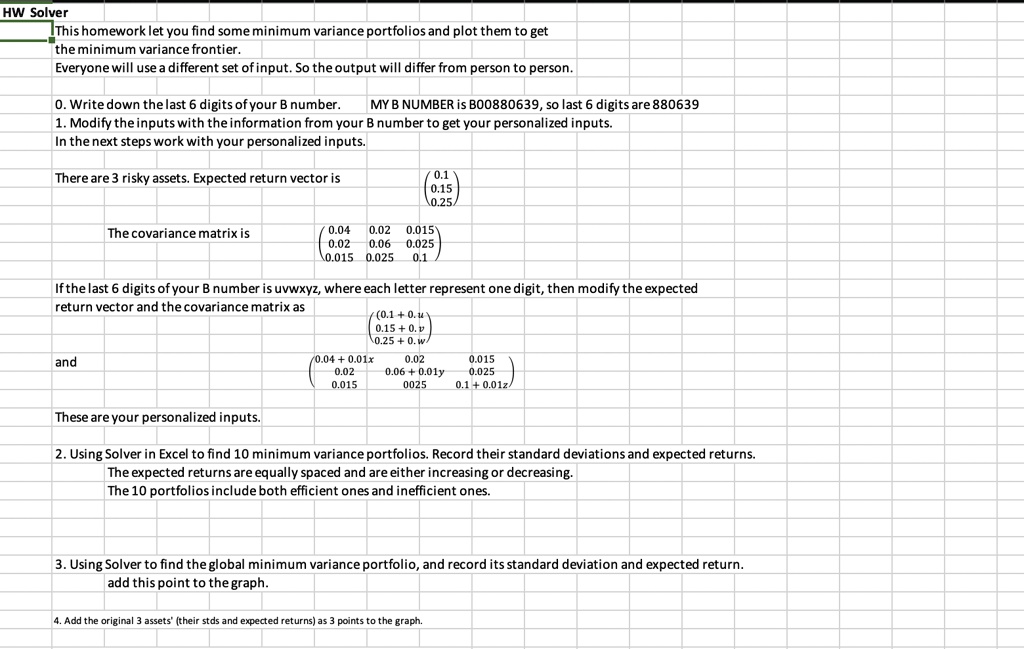

HW Solver

This homework lets you find some minimum variance portfolios and plot them to get the minimum variance frontier. Everyone will use a different set of inputs, so the output will differ from person to person.

0. Write down the last 6 digits of your B number. My B number is B00880639, so the last 6 digits are 880639. Modify the inputs with the information from your B number to get your personalized inputs. In the next steps, work with your personalized inputs.

There are 3 risky assets. The expected return vector is ([0.1],[0.15],[0.25]). The covariance matrix is:

If the last 6 digits of your B number are uvwxyz, where each letter represents one digit, then modify the expected return vector and the covariance matrix as:

([0.1+0.1u, 0.15+0.1v, 0.25+0.1w], [0.04+0.01x, 0.02, 0.015], [0.02, 0.06+0.01y, 0.025], [0.015, 0.025, 0.1+0.01z])

These are your personalized inputs.

Using Solver in Excel to find 10 minimum variance portfolios. Record their standard deviations and expected returns. The expected returns are equally spaced and are either increasing or decreasing. The 10 portfolios include both efficient ones and inefficient ones.

Using Solver to find the global minimum variance portfolio, and record its standard deviation and expected return. Add this point to the graph.

Add the original 3 assets (their standard deviations and expected returns) as 3 points to the graph.