Cost Data

Total Product Average Fixed Cost Average Variable Cost Average Total Cost Marginal Cost

0

1 $ 60.00 $ 45.00 $ 105.00 $ 45

2 30.00 42.50 72.50 40

3 20.00 40.00 60.00 35

4 15.00 37.50 52.50 30

5 12.00 37.00 49.00 35

6 10.00 37.50 47.50 40

7 8.57 38.57 47.14 45

8 7.50 40.63 48.13 55

9 6.67 43.33 50.00 65

10 6.00 46.50 52.50 75

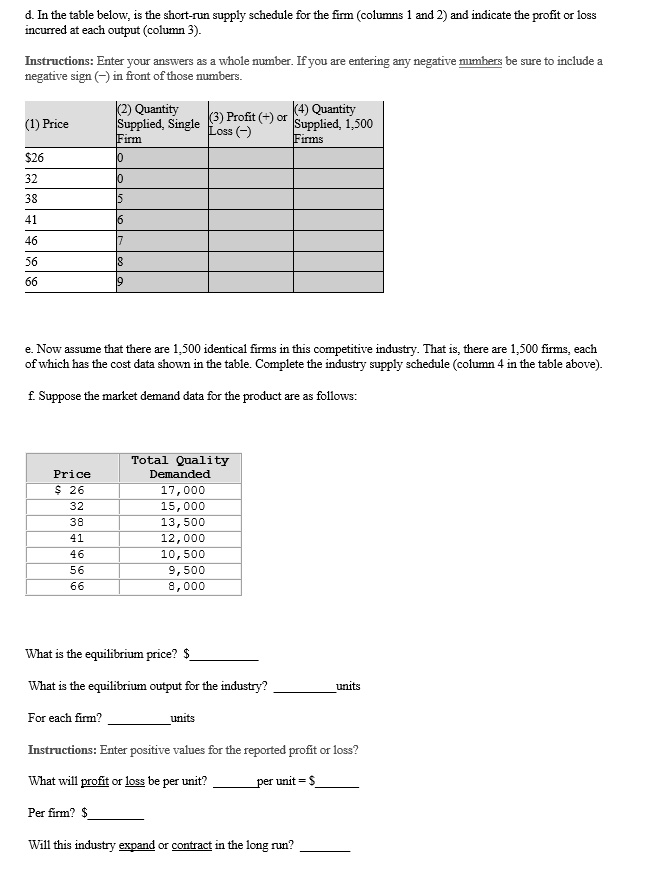

d. In the table below, is the short-run supply schedule for the firm (columns 1 and 2 ) and indicate the profit or loss

incurred at each output (column 3).

Instructions: Enter your answers as a whole number. If you are entering any negative numhers be sure to include a

negative sign ( - ) in front of those numbers.

e. Now assume that there are 1,500 identical firms in this competitive industry. That is, there are 1,500 firms, each

of which has the cost data shown in the table. Complete the industry supply schedule (column 4 in the table above).

f. Suppose the market demand data for the product are as follows:

What is the equilibrium price? $

What is the equilibrium output for the industry?

For each firm?

units

Instructions: Enter positive values for the reported profit or loss?

What will profit or loss be per unit?

per unit =$

Per firm? $

Will this industry expand or contract in the long run?

d. In the table below, is the short-run supply schedule for the firm (columns 1 and 2) and indicate the profit or loss incurred at each output (column 3).

Instructions: Enter your answers as a whole number. If you are entering any negative mumhers be sure to include a negative sign () in front of those numbers.

2) Quantity (4) Quantity (3) Profit (+) or Supplied, Single Supplied, 1,500 Loss () Firm Firms

(1) Price

$26 32 38 41 46 56 66

6

9

e. Now assume that there are 1,500 identical firms in this competitive industry. That is, there are 1,500 firms, each of which has the cost data shown in the table. Complete the industry supply schedule (column 4 in the table above)

f. Suppose the market demand data for the product are as follows:

Total Quality Demanded 17,000 15,000 13,500 12,000 10,500 9,500 8,000

Price $ 26 32 38 41 46 56 66

What is the equilibrium price? $

What is the equilibrium output for the industry?

units

For each firm?

units

Instructions: Enter positive values for the reported profit or loss?

What will profit or loss be per unit?

per unit=S

Per firm? $

Will this industry expand or contract in the long run?