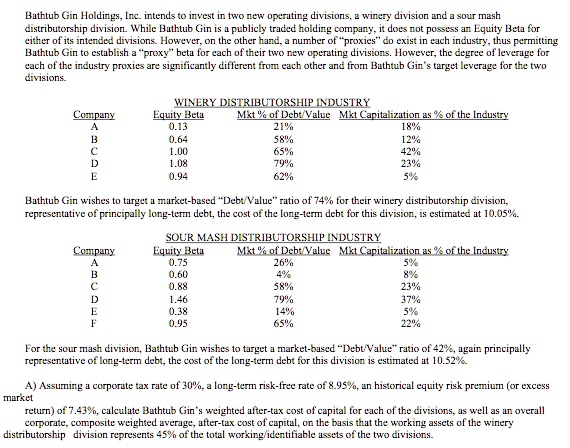

Bathtub Gin Holdings, Inc. intends to invest in two new operating divisions: a winery division and a sour mash distributorship division. While Bathtub Gin is a publicly traded holding company, it does not possess an Equity Beta for either of its intended divisions. However, on the other hand, a number of proxies do exist in each industry, thus permitting Bathtub Gin to establish a proxy beta for each of their two new operating divisions. However, the degree of leverage for each of the industry proxies is significantly different from each other and from Bathtub Gin's target leverage for the two divisions.

WINERY DISTRIBUTORSHIP INDUSTRY

Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry

0.13 21% 18%

0.64 58% 12%

1.00 65% 42%

1.08 79% 23%

0.94 62% 5%

Company A B C D E

Bathtub Gin wishes to target a market-based Debt/Value ratio of 74% for their winery distributorship division, representative of principally long-term debt. The cost of the long-term debt for this division is estimated at 10.05%.

SOUR MASH DISTRIBUTORSHIP INDUSTRY

Equity Beta Mkt % of Debt/Value Mkt Capitalization as % of the Industry

0.75 26% 5%

0.60 4% 8%

0.88 58% 23%

1.46 79% 37%

0.38 14% 5%

0.95 65% 22%

Company A B C D E F

For the sour mash division, Bathtub Gin wishes to target a market-based Debt/Value ratio of 42%, again principally representative of long-term debt. The cost of the long-term debt for this division is estimated at 10.52%.

A) Assuming a corporate tax rate of 30%, a long-term risk-free rate of 8.95%, and a historical equity risk premium (or excess market return) of 7.43%, calculate Bathtub Gin's weighted after-tax cost of capital for each of the divisions, as well as an overall corporate composite weighted average after-tax cost of capital, on the basis that the working assets of the winery distributorship division represent 45% of the total working/identifiable assets of the two divisions.