In providing eccounting scrvices to small businesses, you encounter the following situations.

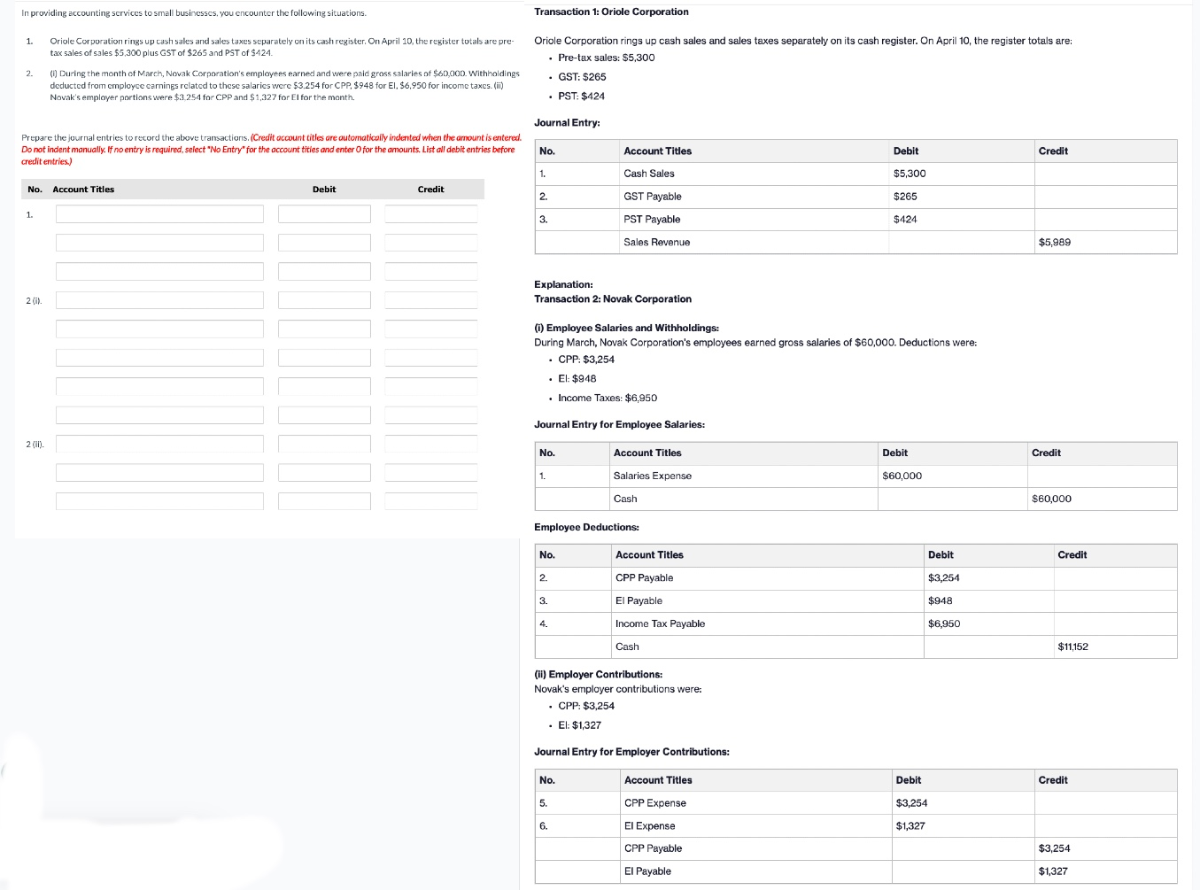

1. Oriole Corporation rings up cash sales and sales taxes separately on its cash register. On April 10 , the resister totals are pretax sales of sales \( \$ 5,300 \) plus GST of \( \$ 265 \) and PST of \( \$ 424 \).

2. (1) During the month of March, Novak Corporation's employees earned and were paid gross salaries of \( \$ 60 \),000. Withhoidings deducted from employce camings related to these salarics were \( \$ 3.254 \) for CPP, \$948 for E1, \( \$ 6,950 \) for income taxes. (ii) Novak's employer portions were \( \$ 3,254 \) for CPP and \( \$ 1,327 \) for EI for the manth.

Prepare the journal entries to record the above transactions. (Credilt occount titles ore outomatically indented when the arnount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account tities and enter O for the anounts. List all debit entries before credit entries.

Transaction 1: Oriole Corporation

Oriole Corporation rings up cash sales and sales taxes separately on its cash register. On April 10, the register totals are:

- Pre-tax sales: \( \$ 5,300 \)

- GST: \( \$ 265 \)

. PST: \( \$ 424 \)

Journal Entry:

\begin{tabular}{|c|c|c|c|}

\hline No. & Account Titles & Debit & Credit \\

\hline 1. & Cash Sales & \( \$ 5,300 \) & \\

\hline \multirow[t]{2}{*}{3.} & PST Payable & \( \$ 424 \) & \\

\hline & Sales Revenue & & \( \$ 5,989 \) \\

\hline

\end{tabular}

Explanation:

Transaction 2: Novak Corporation

(i) Employee Salaries and Withholdings:

During March, Novak Corporation's employees earned gross salaries of \( \$ 60,000 \). Deductions were:

- CPP: \( \$ 3,254 \)

- El: \( \$ 948 \)

- Income Taxes: \( \$ 6,950 \)

Journal Entry for Employee Salaries:

\begin{tabular}{|l|l|l|l|}

\hline No. & Account Titles & Debit & Credit \\

\hline 1. & Salaries Expense & \( \$ 60,000 \) & \\

\hline & Cash & & \( \$ 60,000 \) \\

\hline

\end{tabular}

Employee Deductions:

\begin{tabular}{|l|l|l|l|}

\hline No. & Account Titles & Debit & Credit \\

\hline 2. & CPP Payable & \( \$ 3,254 \) & \\

\hline 3. & El Payable & \( \$ 948 \) & \\

\hline 4. & Income Tax Payable & \( \$ 6,950 \) & \\

\hline & Cash & & \( \$ 11,152 \) \\

\hline

\end{tabular}

(ii) Employer Contributions:

Novak's employer contributions were:

- CPP: \( \$ 3,254 \)

- El: \( \$ 1,327 \)

Journal Entry for Employer Contributions:

\begin{tabular}{|l|l|l|l|}

\hline No. & Account Titles & Debit & Credit \\

\hline 5. & CPP Expense & \( \$ 3,254 \) & \\

\hline 6. & EI Expense & \( \$ 1,327 \) & \\

\hline & CPP Payable & & \( \$ 3,254 \) \\

\hline & El Pryable & & \( \$ 1,327 \) \\

\hline

\end{tabular}