Inventory Analysis of Nucor

Nucor is one of the largest U.S. steel companies. The attached Exhibit contains financial data for the five years ended December 31, 1995. Nucor has used the LIFO method for all inventories during the entire time period. There were no LIFO liquidations.

The objective of this assignment is to show the impact of Nucor’s use of the LIFO inventory method on its:

1. Balance sheet

2. Income statement

3. Cash flow from operations

4. Financial ratios

Required:

The following questions should be answered using the data provided in the adjoining Exhibit:

1. Calculate gross margin (both $ and as a percent of sales) under both the LIFO and FIFO methods for the years 1990 to 1995.

Discuss the differences in the level, trend, and variability of gross margins under the two methods. Which method gives a more realistic estimate of Nucor’s ability to cover its cost of production?

2. Calculate net income, assuming Nucor had used the FIFO methods of reporting for 1990 to 1995, and discuss differences in the level, growth rate, and variability of net income under the two methods. Which method provides a more realistic measure of Nucor’s profitability?

3. Calculate Nucor’s cash flow from operations, assuming Nucor had used the FIFO method of reporting for 1990 to 1995. Compare your results to reported cash from operations and discuss the difference in level and growth rate.

4. Calculate stockholders’ equity per share, stating inventories at FIFO. Compare your results to reported equity and discuss the difference in level and growth rate.

5. Calculate the following ratios for Nucor, using both reported data (LIFO), FIFO and current cost (FIFO for inventory balance and LIFO for COPS), for 1990 to 1995:

• Current ratio

• Return on (average) equity (ROE)

Discuss the effect of using LIFO on the level and variability of both ratios.

6. Calculate Nucor’s inventory turnover ratios for 1990 to 1995 using:

(a) LIFO data

(b) FIFO data

(c) Current Cost (FIFO for inventory balance and LIFO for COPS) Discuss the differences among these turnover ratios and select the method that provides the best measure of true economic turnover. Discuss the trend in Nucor’s inventory turnover over the 1990 to 1995 period and factors that might account for the variability of reported turnover.

7. Using the results of Question 1 through 7 and the data in Exhibit, discuss the advantages and disadvantages to Nucor of using the LIFO method over the 1990 to 1995 time period

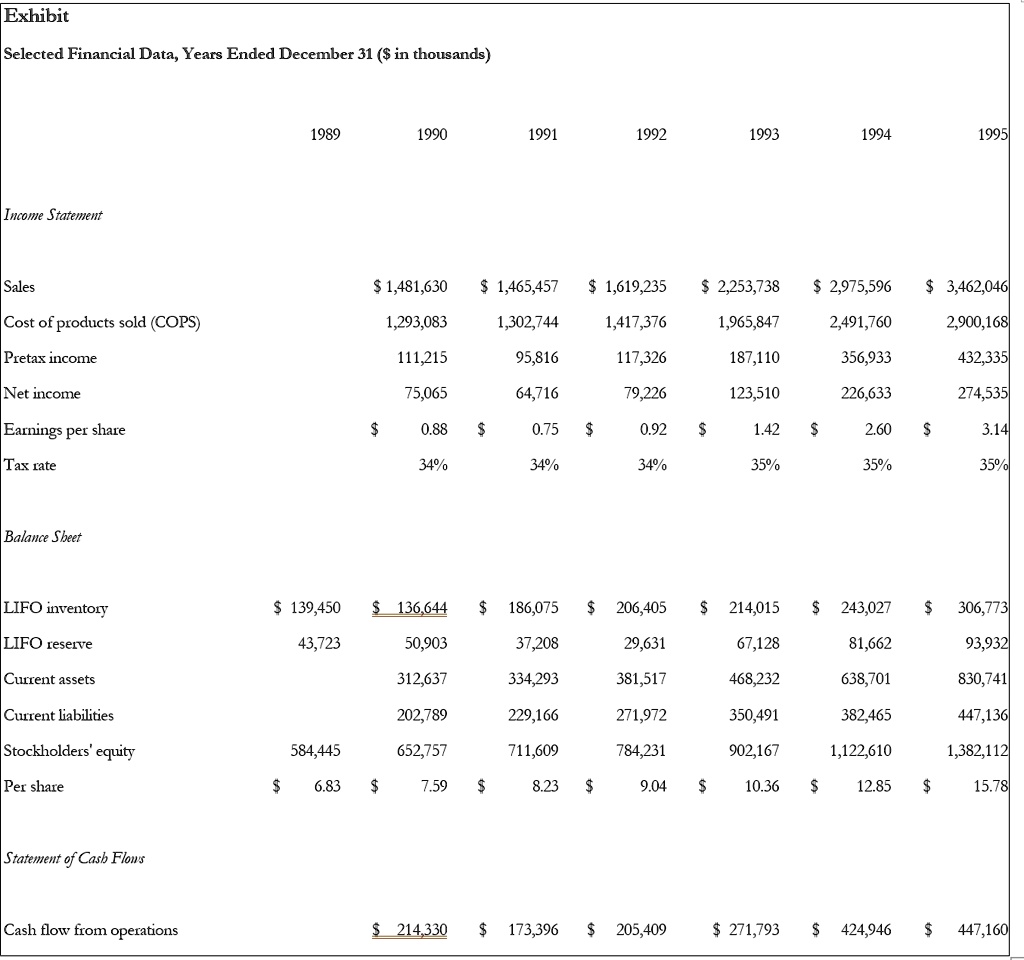

Exhibit

Selected Financial Data, Years Ended December 31 ($ in thousands)

1989

1990

1991

1992

1993

1994

1995

Income Statement

Sales

$1,481,630

$1,465,457

$1,619,235

$2,253,738

$2,975,596

$3,462,046

Cost of products sold (COPS)

$1,293,083

$1,302,744

$1,417,376

$1,965,847

$2,491,760

$2,900,168

Pretax income

$111,215

$95,816

$117,326

$187,110

$356,933

$432,335

Net income

$75,065

$64,716

$79,226

$123,510

Earnings per share

$0.88

$0.75

$0.92

$1.42

Tax rate

34%

34%

34%

35%

35%

35%

Balance Sheet

LIFO inventory

$139,450

$136,644

$186,075

$206,405

$214,015

$243,027

$306,773

LIFO reserve

$43,723

$50,903

$37,208

$334,293

$229,166

$711,609

$29,631

$381,517

$67,128

$81,662

$93,932

$830,741

Current assets

$312,637

$468,232

$638,701

Current liabilities

$202,789

$271,972

$350,491

$902,167

$382,465

$447,136

Stockholders' equity

$584,445

$652,757

$784,231

$1,122,610

$1,382,112

Per share

$6.83

$7.59

$8.23

$9.04

$12.85

$15.78

Statement of Cash Flows

Cash flow from operations

$214,330

$173,396

$205,409

$271,793

$424,946

$447,160