Journalize issuance of the bonds and the first semiannual interest payment under each of the following three assumptions. The

company amortizes bond premium and discount by the effective-interest amortization method. Explanations are not required. (Round

to the nearest dollar.)

View the bond assumptions.

(Record debits first, then credits. Exclude explanations from any journal entries. Round your final answers to the nearest

whole dollar.)

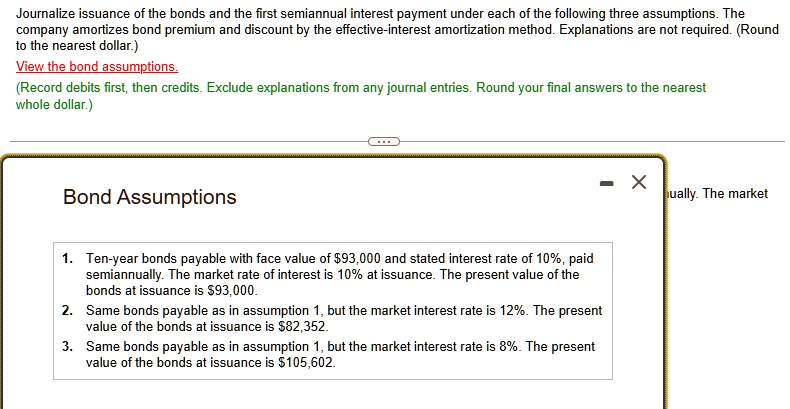

Bond Assumptions

1. Ten-year bonds payable with face value of $93,000 and stated interest rate of 10%, paid

semiannually. The market rate of interest is 10% at issuance. The present value of the

bonds at issuance is $93,000.

2. Same bonds payable as in assumption 1, but the market interest rate is 12%. The present

value of the bonds at issuance is $82,352.

3. Same bonds payable as in assumption 1, but the market interest rate is 8%. The present

value of the bonds at issuance is $105,602.