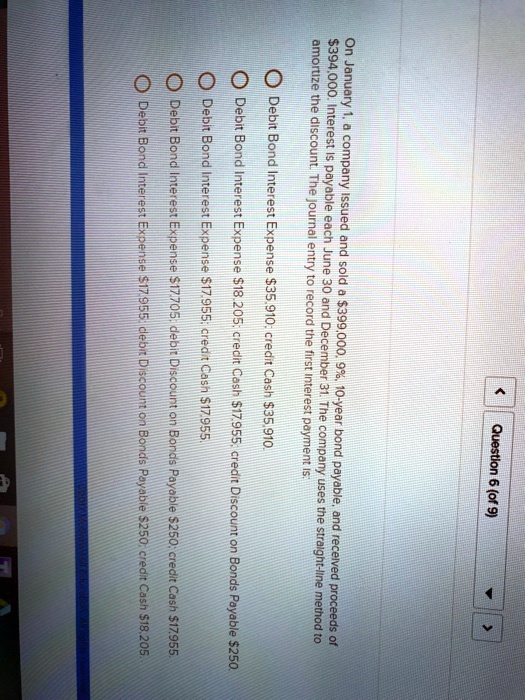

On January 1, a company issued and sold a $399,000, 9%, 10-year bond payable, and received proceeds of

$394,000. Interest is payable each June 30 and December 31. The company uses the straight-line method to

amortize the discount. The journal entry to record the first interest payment is:

Debit Bond Interest Expense $35,910; credit Cash $35,910.

Debit Bond Interest Expense $18,205; credit Cash $17,955; credit Discount on Bonds Payable $250.

Debit Bond Interest Expense $17,955; credit Cash $17,955.

Debit Bond Interest Expense $17,705; debit Discount on Bonds Payable $250; credit Cash $17,955.

Debit Bond Interest Expense $17,955; debit Discount on Bonds Payable $250; credit Cash $18,205.