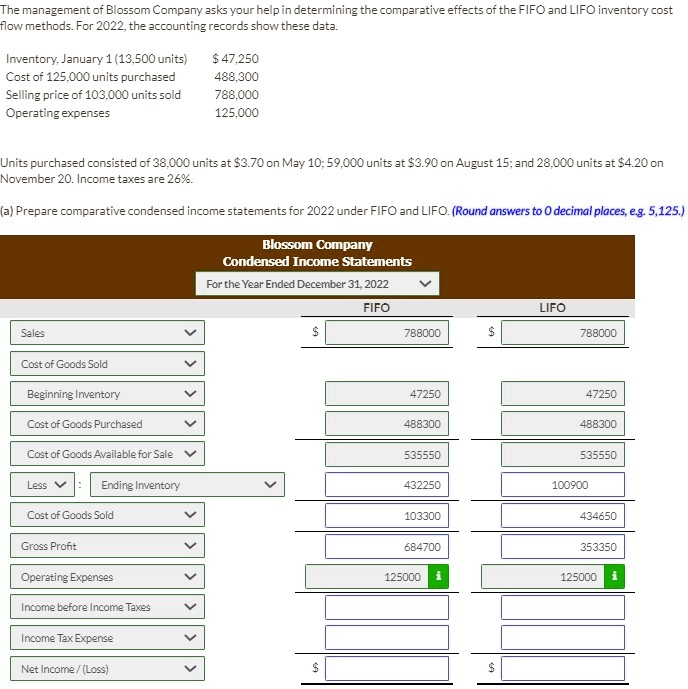

The management of Blossom Company asks your help in determining the comparative effects of the FIFO and LIFO inventory cost

flow methods. For 2022, the accounting records show these data.

Inventory, January 1 (13,500 units)

$ 47,250

Cost of 125,000 units purchased

488,300

Selling price of 103,000 units sold

788,000

Operating expenses

125,000

Units purchased consisted of 38,000 units at $3.70 on May 10; 59,000 units at $3.90 on August 15; and 28,000 units at $4.20 on

November 20. Income taxes are 26%.

(a) Prepare comparative condensed income statements for 2022 under FIFO and LIFO. (Round answers to 0 decimal places, e.g. 5,125.)

Blossom Company

Condensed Income Statements

For the Year Ended December 31, 2022

FIFO

LIFO

$ 788000

$ 788000

Sales

Cost of Goods Sold

Beginning Inventory

47250

47250

Cost of Goods Purchased

488300

488300

Cost of Goods Available for Sale

535550

535550

Less

Ending Inventory

432250

100900

Cost of Goods Sold

103300

434650

Gross Profit

684700

353350

Operating Expenses

125000

125000

Income before Income Taxes

Income Tax Expense

Net Income/(Loss)

$

$