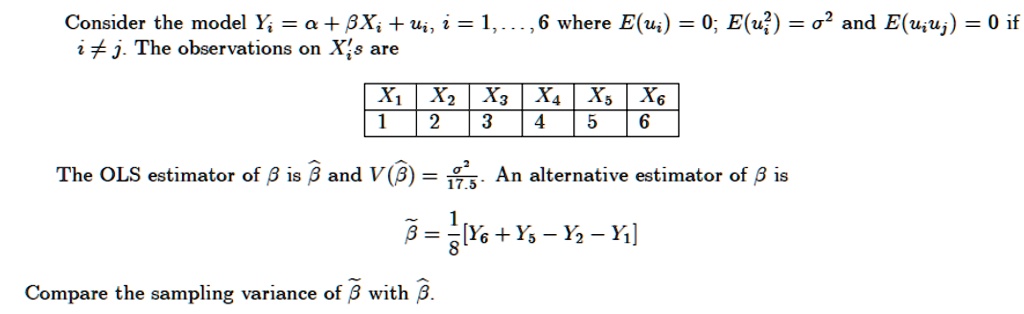

Consider the model $Y_i = \alpha + \beta X_i + u_i$, $i = 1, \dots, 6$ where $E(u_i) = 0$; $E(u_i^2) = \sigma^2$ and $E(u_i u_j) = 0$ if $i \neq j$. The observations on $X_i$'s are

$X_1$ $X_2$ $X_3$ $X_4$ $X_5$ $X_6$

1 2 3 4 5 6

The OLS estimator of $\beta$ is $\hat{\beta}$ and $V(\hat{\beta}) = \frac{\sigma^2}{17.5}$. An alternative estimator of $\beta$ is

$\tilde{\beta} = \frac{1}{8}[Y_6 + Y_5 - Y_2 - Y_1]$

Compare the sampling variance of $\tilde{\beta}$ with $\hat{\beta}$.