Question 1

The following information is provided for a stock market in which asset returns respond to two factors:

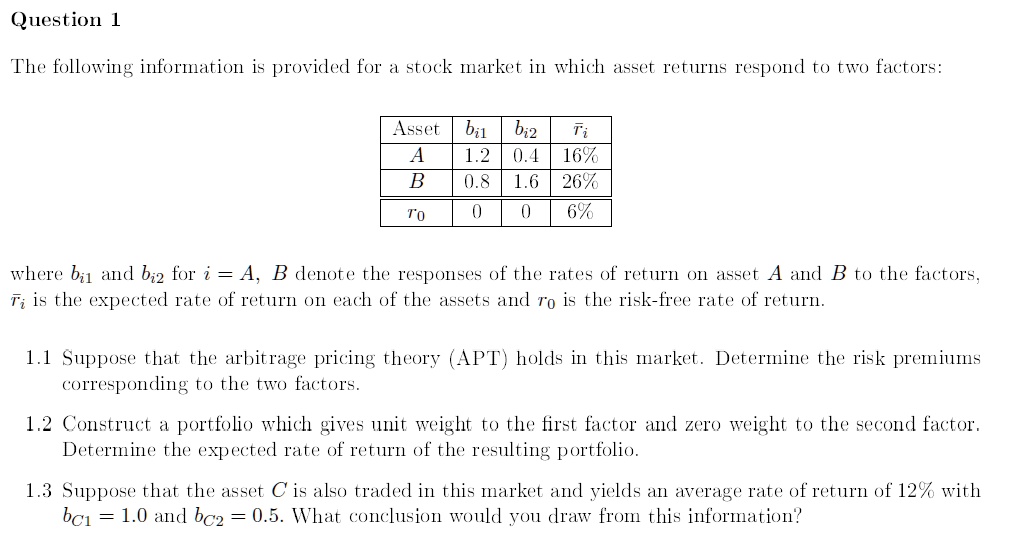

Asset $b_{i1}$ $b_{i2}$ $\bar{r}_{i}$

A 1.2 0.4 16%

B 0.8 1.6 26%

$r_{0}$ 0 0 6%

where $b_{i1}$ and $b_{i2}$ for $i = A, B$ denote the responses of the rates of return on asset $A$ and $B$ to the factors, $\bar{r}_{i}$ is the expected rate of return on each of the assets and $r_{0}$ is the risk-free rate of return.

1.1 Suppose that the arbitrage pricing theory (APT) holds in this market. Determine the risk premiums corresponding to the two factors.

1.2 Construct a portfolio which gives unit weight to the first factor and zero weight to the second factor. Determine the expected rate of return of the resulting portfolio.

1.3 Suppose that the asset $C$ is also traded in this market and yields an average rate of return of 12% with $b_{C1} = 1.0$ and $b_{C2} = 0.5$. What conclusion would you draw from this information?