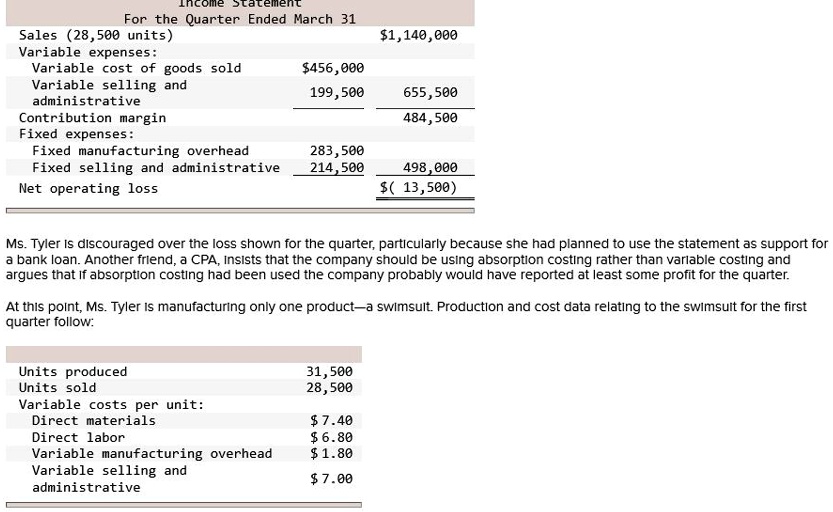

Income Statement

For the Quarter Ended March 31

Sales (28,500 units)

$1,140,000

Variable expenses:

Variable cost of goods sold

$456,000

Variable selling and

199,500

655,500

administrative

Contribution margin

484,500

Fixed expenses:

Fixed manufacturing overhead

283,500

Fixed selling and administrative

214,500

498,000

Net operating loss

$(13,500)

Ms. Tyler is discouraged over the loss shown for the quarter, particularly because she had planned to use the statement as support for

a bank loan. Another friend, a CPA, insists that the company should be using absorption costing rather than variable costing and

argues that if absorption costing had been used the company probably would have reported at least some profit for the quarter.

At this point, Ms. Tyler is manufacturing only one product—a swimsuit. Production and cost data relating to the swimsuit for the first

quarter follow:

Units produced

31,500

Units sold

28,500

Variable costs per unit:

Direct materials

$7.40

Direct labor

$6.80

Variable manufacturing overhead

$1.80

Variable selling and

$7.00

administrative