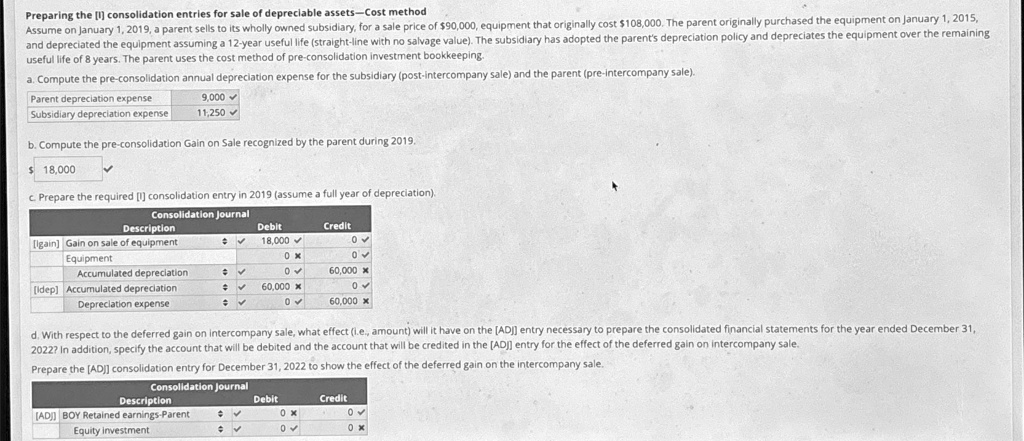

Preparing the [I] consolidation entries for sale of depreciable assets-Cost method useful life of 8 years. The parent uses the cost method of pre-consolidation investment bookkeeping.

a. Compute the pre-consolidation annual depreciation expense for the subsidiary (post-intercompany sale) and the parent (pre-intercompany sale).

able[[Parent depreciation expense,9,000vv

Preparing the [I] consolidation entries for sale of depreciable assets-Cost method Assume on January 1,2019,a parent sells to its wholly owned subsidiary,for a sale price of $90,000,equipment that originally cost $108,000.The parent originally purchased the equipment on January 1,2015, and depreciated the equipment assuming a 12-year useful life straight-line with no salvage value.The subsidiary has adopted the parent's depreciation policy and depreciates the equipment over the remaining useful life of 8 years. The parent uses the cost method of pre-consolidation investment bookkeeping. a.Compute the pre-consolidation annual depreciation expense for the subsidiary (post-intercompany sale) and the parent(pre-intercompany sale). Parent depreciation expense 9,000 Subsidiary depreciation expense 11,250

b.Compute the pre-consolidation Gain on Sale recognized by the parent during 2019

$18,000

c.Prepare the required [1] consolidation entry in 2019assume a full year of depreciation Consolidation Journal Debit Credit [Igain][Gain on sale of equipment 18,000 Ov Equipment 0x O'v Accumulated depreciation OV 60,000 [Idep]Accumulated depreciation 60,000x OV Depreciation expense 0V 60,000

2022 In addition, specify the account that will be debited and the account that will be credited in the [AD] entry for the effect of the deferred gain on intercompany sale. Prepare the [ADJ] consolidation entry for December31,2022 to show the effect of the deferred gain on the intercompany sale.

Description

Debit v 0x

Credit

[AD]BOY Retained earnings-Parent Equity investment

0x