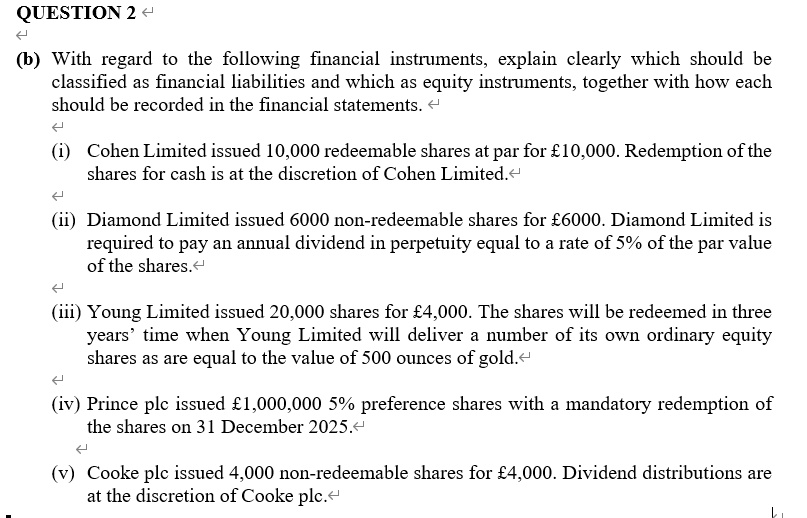

QUESTION 2

?

(b) With regard to the following financial instruments, explain clearly which should be

classified as financial liabilities and which as equity instruments, together with how each

should be recorded in the financial statements. ?

?

(i) Cohen Limited issued 10,000 redeemable shares at par for £10,000. Redemption of the

shares for cash is at the discretion of Cohen Limited.

(ii) Diamond Limited issued 6000 non-redeemable shares for £6000. Diamond Limited is

required to pay an annual dividend in perpetuity equal to a rate of 5% of the par value

of the shares.

?

(iii) Young Limited issued 20,000 shares for £4,000. The shares will be redeemed in three

years' time when Young Limited will deliver a number of its own ordinary equity

shares as are equal to the value of 500 ounces of gold.?

(iv) Prince plc issued £1,000,000 5% preference shares with a mandatory redemption of

the shares on 31 December 2025.

(v) Cooke plc issued 4,000 non-redeemable shares for £4,000. Dividend distributions are

at the discretion of Cooke plc.