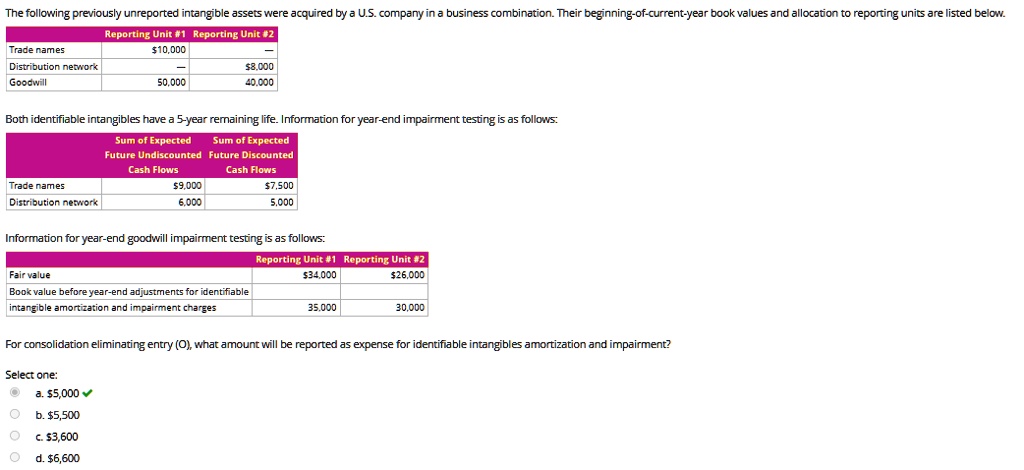

The following previously unreported intangible assets were acquired by a U.S. company in a business combination. Their beginning-of-current-year book values and allocation to reporting units are listed below.

Trade names

Distribution network

Goodwill

Reporting Unit #1 Reporting Unit #2

$10,000

50,000

$8,000

40,000

Both identifiable intangibles have a 5-year remaining life. Information for year-end impairment testing is as follows:

Sum of Expected Sum of Expected

Future Undiscounted Future Discounted

Cash Flows

Cash Flows

Trade names

Distribution network

$9,000

6,000

$7,500

5,000

Information for year-end goodwill impairment testing is as follows:

Reporting Unit #1 Reporting Unit #2

Fair value

$34,000

$26,000

Book value before year-end adjustments for identifiable

intangible amortization and impairment charges

35,000

30,000

For consolidation eliminating entry (O), what amount will be reported as expense for identifiable intangibles amortization and impairment?

Select one:

a. $5,000

b. $5,500

c. $3,600

d. $6,600