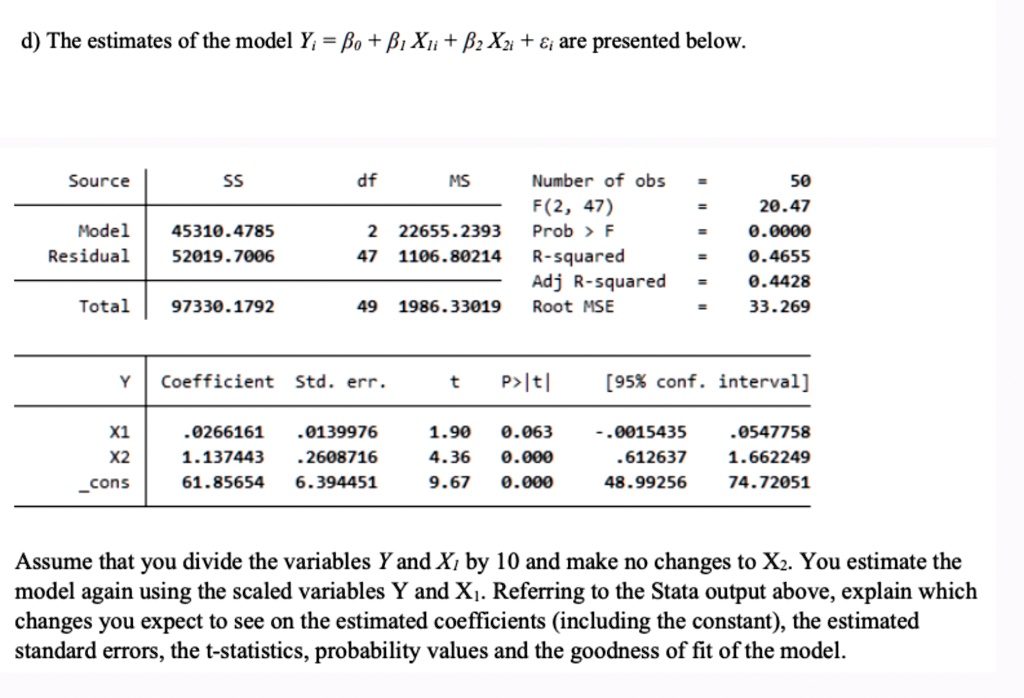

d) The estimates of the model Y_(i)=�eta _(0)+�eta _(1)x_(1i)+�eta _(2)x_(2i)+epsi _(i) are presented below.

Assume that you divide the variables Y and x_(l) by 10 and make no changes to x_(2). You estimate the

model again using the scaled variables Y and x_(1). Referring to the Stata output above, explain which

changes you expect to see on the estimated coefficients (including the constant), the estimated

standard errors, the t-statistics, probability values and the goodness of fit of the model.

d) The estimates of the model Y; = o + X + Xi + &; are presented below.

Source

ss

dp

MS

Number of obs F(2,47) Prob > F R-squared Adj R-squared Root MSE

50 20.47 0.0000 0.4655 0.4428 33.269

=

Model Residual

45310.4785 52019.7006

2 22655.2393 47 1106.80214

Total

97330.1792

49 1986.33019

Y

Coefficient Std.err.

t

P>|t|

[95% conf.interval]

X1 X2 _cons

.0266161 1.137443 61.85654

.0139976 .2608716 6.394451

1.90 4.36 9.67

0.063 0.000 0.000

-.0015435 .612637 48.99256

.0547758 1.662249 74.72051

Assume that you divide the variables Y and X by 10 and make no changes to X2. You estimate the model again using the scaled variables Y and X.. Referring to the Stata output above, explain which changes you expect to see on the estimated coefficients (including the constant), the estimated standard errors, the t-statistics, probability values and the goodness of fit of the model.