7.

Does a firm's price equal the minimum of average total cost in the short run, in the long run, or

both? Explain./2

8.

You go out to the best restaurant in town and order a lobster dinner for $40. After eating half of

the lobster, you realize that you are quite full. Your date wants you to finish your dinner, because

you can't take it home and because \"you've already paid for it.\" What should you do? Relate

your answer to the material in this chapter. /2

9.

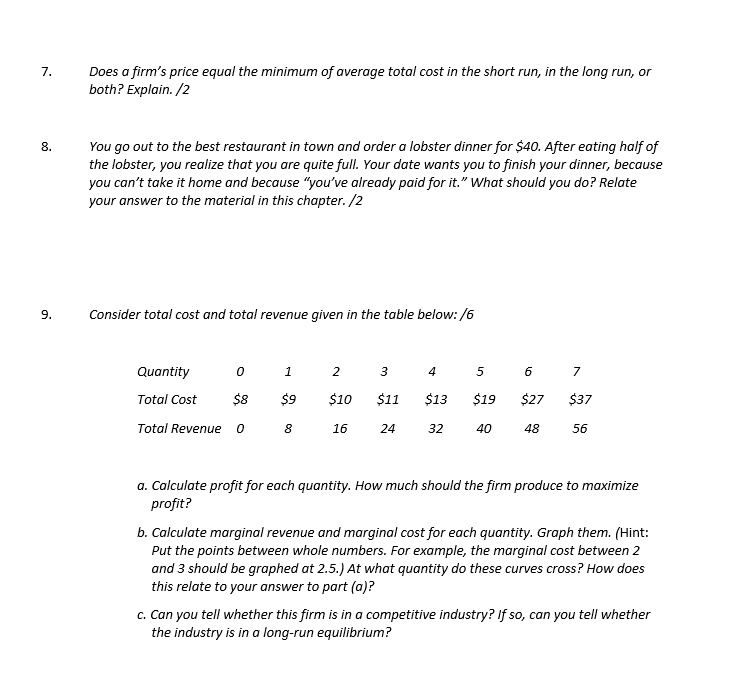

Consider total cost and total revenue given in the table below: /6

Quantity

0

1

2

3

4

5

6

7

Total Cost $8

$9

$10 $11

$13

$19

$27 $37

Total Revenue 0

8

16

24

32

40

48 56

a. Calculate profit for each quantity. How much should the firm produce to maximize

profit?

b. Calculate marginal revenue and marginal cost for each quantity. Graph them. (Hint:

Put the points between whole numbers. For example, the marginal cost between 2

and 3 should be graphed at 2.5.) At what quantity do these curves cross? How does

this relate to your answer to part (a)?

c. Can you tell whether this firm is in a competitive industry? If so, can you tell whether

the industry is in a long-run equilibrium?