Texts: Question list

K

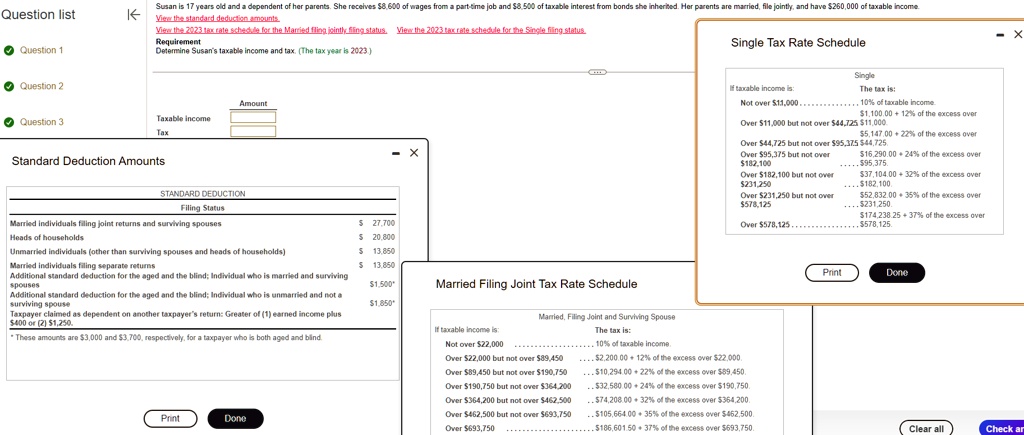

Susan is 17 years old and a dependent of her parents. She receives $8,600 of wages from a part-time job and $8,500 of taxable interest from bonds she inherited. Her parents are married, file jointly, and have $260,000 of taxable income. View the standard deduction amounts. View the 2023 tax rate schedule for the Married filing jointly filing status. View the 2023 tax rate schedule for the Single filing status. Requirement: Single Tax Rate Schedule. Determine Susan's taxable income and tax. (The tax year is 2023.)

X

Question 1

Single: If taxable income is: The tax is: Not over $11,000.. .. 10% of taxable income $1,100.00 + 12% of the excess over $11,000. Over $11,000 but not over $44,725 $5,147.00 + 22% of the excess over $11,000. Over $44,725 but not over $95,375 $44,725. Over $95,375 but not over $182,100 $16,290.00 + 24% of the excess over $95,375. Over $182,100 but not over $231,250 $37,104.00 + 32% of the excess over $182,100. Over $231,250 but not over $578,125 $231,250 $174,238.25 + 37% of the excess over $231,250. Over $578,125... ...$578,125.

Question 2

Taxable income: Tax:

Question 3

Standard Deduction Amounts

STANDARD DEDUCTION Filing Status

Married individuals filing joint returns and surviving spouses: $27,700

Heads of households: $20,800

Unmarried individuals (other than surviving spouses and heads of households): $13,850

Married individuals filing separate returns: $13,850

Additional standard deduction for the aged and the blind; Individual who is married and surviving spouses: $1,500*

Additional standard deduction for the aged and the blind; Individual who is unmarried and not a surviving spouse: $1,850*

Taxpayer claimed as dependent on another taxpayer's return: Greater of (1) earned income plus $400 or (2) $1,250

*These amounts are $3,000 and $3,700, respectively, for a taxpayer who is both aged and blind.

Print

Done

Married Filing Joint Tax Rate Schedule

Married, Filing Joint and Surviving Spouse: If taxable income is: The tax is: Not over $22,000 ........10% of taxable income Over $22,000 but not over $89,450 ...$2,200.00 + 12% of the excess over $22,000 Over $89,450 but not over $190,750 ...$10,294.00 + 22% of the excess over $89,450 Over $190,750 but not over $364,200 $32,580.00 + 24% of the excess over $190,750 Over $364,200 but not over $462,500 $74,208.00 + 32% of the excess over $364,200 Over $462,500 but not over $693,750 $105,664.00 + 35% of the excess over $462,500 Over $693,750 $186,601.50 + 37% of the excess over $693,750.

Print

Clear all