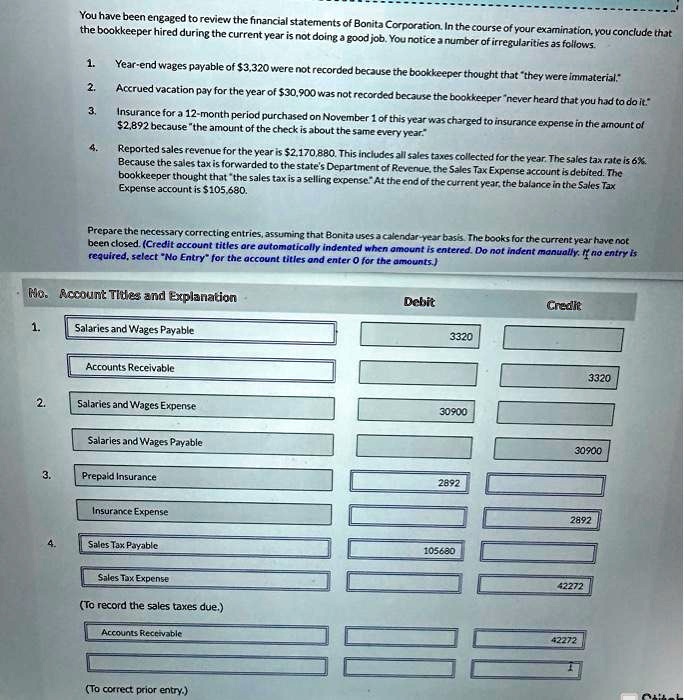

You have been engaged to review the financial statements of Bonita Corporation. In the course of your examination, you conclude that

the bookkeeper hired during the current year is not doing a good job. You notice a number of irregularities as follows.

1.

Year-end wages payable of $3,320 were not recorded because the bookkeeper thought that "they were immaterial."

2.

Accrued vacation pay for the year of $30,900 was not recorded because the bookkeeper "never heard that you had to do it."

3.

Insurance for a 12-month period purchased on November 1 of this year was charged to insurance expense in the amount of

$2,892 because "the amount of the check is about the same every year."

4.

Reported sales revenue for the year is $2,170,880. This includes all sales taxes collected for the year. The sales tax rate is 6%.

Because the sales tax is forwarded to the state's Department of Revenue, the Sales Tax Expense account is debited. The

bookkeeper thought that "the sales tax is a selling expense." At the end of the current year, the balance in the Sales Tax

Expense account is $105,680.

Prepare the necessary correcting entries, assuming that Bonita uses a calendar-year basis. The books for the current year have not

been closed. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is

required, select "No Entry" for the account titles and enter 0 for the amounts.)

No. Account Titles and Explanation

Debit

Credit

1.

Salaries and Wages Payable

3320

Accounts Receivable

3320

2.

Salaries and Wages Expense

30900

Salaries and Wages Payable

30900

3.

Prepaid Insurance

2892

Insurance Expense

2892

4.

Sales Tax Payable

105680

Sales Tax Expense

(To record the sales taxes due.)

Accounts Receivable

42272

(To correct prior entry.)

42272